The collapse of hyperinflation begins when people stop believing the next banknote will buy anything tomorrow.

That is the moment the monetary system stops functioning as money and starts behaving like a political rumour printed on paper. Prices rise not simply because goods are scarce, but because trust has disappeared. Workers rush wages into food. Shopkeepers rewrite prices during the day. Governments issue larger notes while their authority shrinks. The question, then, is not only what caused the collapse of hyperinflation. The deeper question is what finally stopped the collapse of money itself. Across Weimar Germany, Hungary, Bolivia and Zimbabwe, the answer is consistent: hyperinflation ended when governments cut the link between public deficits and the printing press, introduced a credible monetary anchor, and forced society to believe that the new money would not be destroyed like the old.

Quick Answer: What Caused the Collapse of Hyperinflation?

Hyperinflation collapsed when governments broke the mechanism that was creating it. In most historical cases, the immediate mechanism was the same: a state could not fund itself through normal taxation or borrowing, so it financed spending by creating money. Once households and businesses realised that new money would keep flooding the economy, they tried to escape the currency. That escape accelerated the price spiral.

The collapse ended only when a credible replacement system arrived. In Weimar Germany, the Rentenmark was introduced in November 1923 in strictly limited quantities and backed by mortgages on industrial and agricultural assets. In Hungary, the pengo was replaced by the forint in 1946. In Bolivia, the 1985 New Economic Policy attacked the fiscal deficit and reset the exchange-rate regime. In Zimbabwe, hyperinflation stopped after the Zimbabwe dollar effectively died, and foreign currencies became the working money of the economy. The practical lesson is clear: hyperinflation is not solved by printing a higher-denomination note. It is solved by restoring credible limits.

The Moment Money Stops Being Money

Every hyperinflation story begins with a state under pressure. War debts, reparations, collapsed production, lost tax capacity, external debt, political crisis, or sanctions weaken the government’s balance sheet. At first, inflation can look manageable. Prices rise. Wages adjust. Ministers blame speculators, shortages or foreign enemies. But once the public believes that the state will meet every bill with new money, the currency begins to lose its three core functions.

First, it stops being a reliable store of value. A worker paid on Friday knows the wage will buy less by Monday. Second, it stops being a useful unit of account. A price list becomes obsolete almost as soon as it is printed. Third, it stops being a trusted medium of exchange. People prefer dollars, gold, cigarettes, food, fuel, land, tools or anything that cannot be multiplied by decree.

This is why the classic Cagan threshold of hyperinflation - a monthly price increase above 50% - matters. It is not just a statistic. It marks a phase where prices can compound at a speed that destroys normal economic calculation. Businesses cannot budget. Credit markets vanish. Taxes lose value between assessment and collection. The state prints more to cover the revenue shortfall. That printing weakens the currency further. The loop feeds on itself.

The Common Cause: Fiscal Collapse Meets the Printing Press

A budget problem becomes a monetary disaster

Hyperinflation is often described as excessive money printing, but that is only the visible symptom. The engine is usually in a state of fiscal collapse. A government has obligations it cannot finance through taxes, bonds or credible external borrowing. When the central bank becomes the financing arm of the treasury, the budget deficit migrates into the money supply.

In Weimar Germany, the post-war state carried domestic political obligations, reparations pressure and the economic shock of the Ruhr crisis. In Hungary after the Second World War, destruction, reparations and public spending overwhelmed the fiscal position. In Bolivia during the early 1980s, public deficits, external debt pressure and weak fiscal institutions created the monetary conditions for the 1985 crisis. In Zimbabwe, falling output and state-directed spending collided with a collapsing tax base and an increasingly discredited currency.

Confidence disappears before the banknotes do

Once confidence breaks, the public tries to reduce exposure to the domestic currency. That behaviour increases the velocity of money. A note may pass through several hands in a day because nobody wants to hold it overnight. Prices rise not only because more money exists, but because the same money is being spent faster. The more people flee the currency, the harder the government must print to buy real goods and services.

This makes hyperinflation a political economy crisis rather than a narrow monetary event. The state cannot order trust back into existence. It has to change the incentives that destroyed trust in the first place.

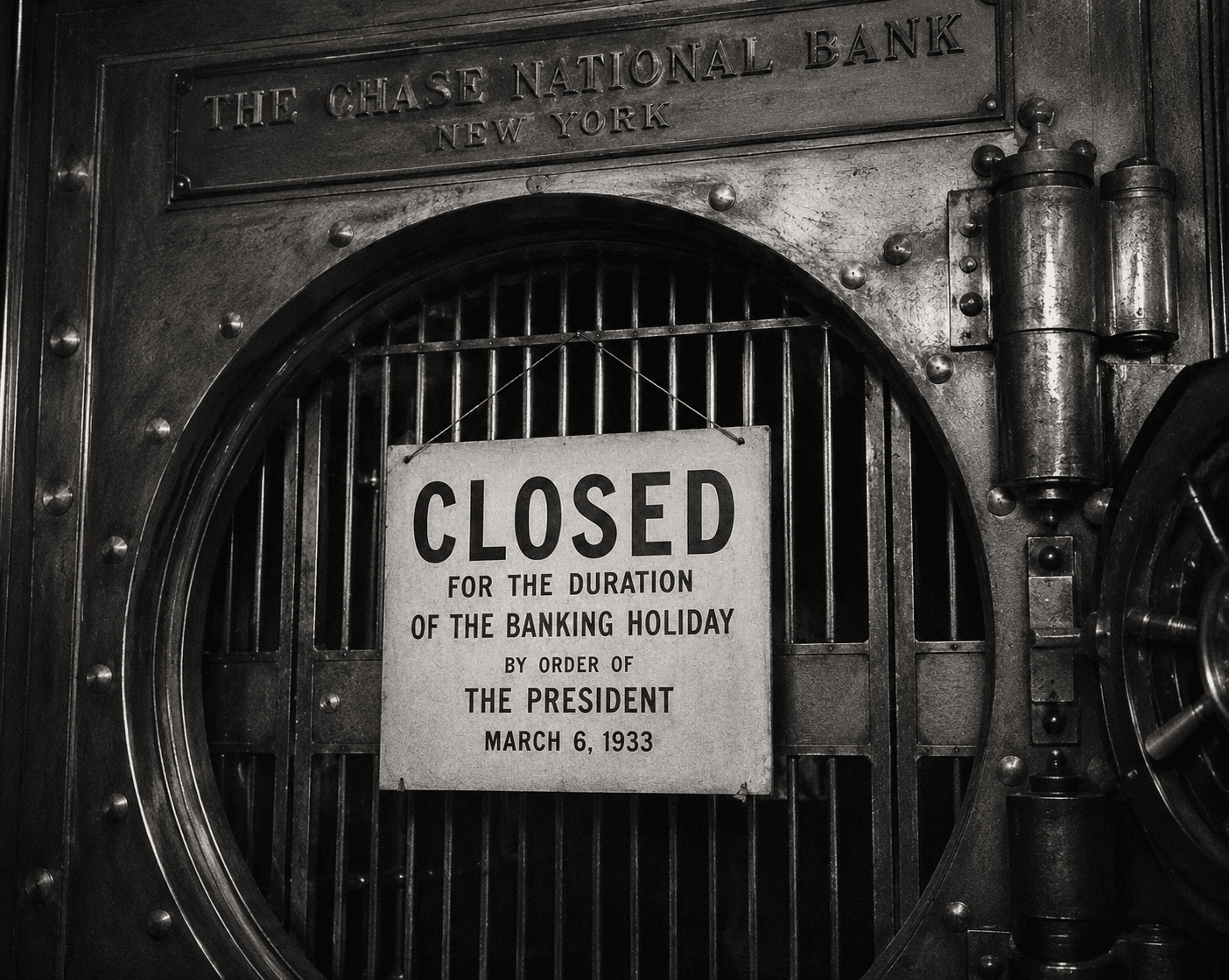

Weimar Germany: When the Rentenmark Rebuilt Trust

In 1923, Germany became the textbook image of hyperinflation because the collapse was visible in everyday life. Wages were paid more frequently. Prices rose at a frightening speed. The old paper mark no longer gave people a reason to wait. Holding cash became a punishment.

The Weimar crisis did not end because the old mark recovered. It ended because the old logic was broken. The Rentenmark was introduced in November 1923 in limited quantities and backed by a mortgage on industrial and agricultural resources. It was not a magical object. Its power came from the political signal behind it: the government would no longer treat the printing press as an unlimited fiscal instrument.

The public response was striking. The new currency worked because it combined scarcity, institutional change and a story people could understand. The old mark represented chaos. The Rentenmark represented a line in the sand. When that line was defended, prices stabilised.

The lesson is not that land backing automatically solves inflation. The deeper lesson is that a currency anchor must be believable. People will not trust money because a minister announces a reform. They trust it when the reform changes the behaviour of the state.

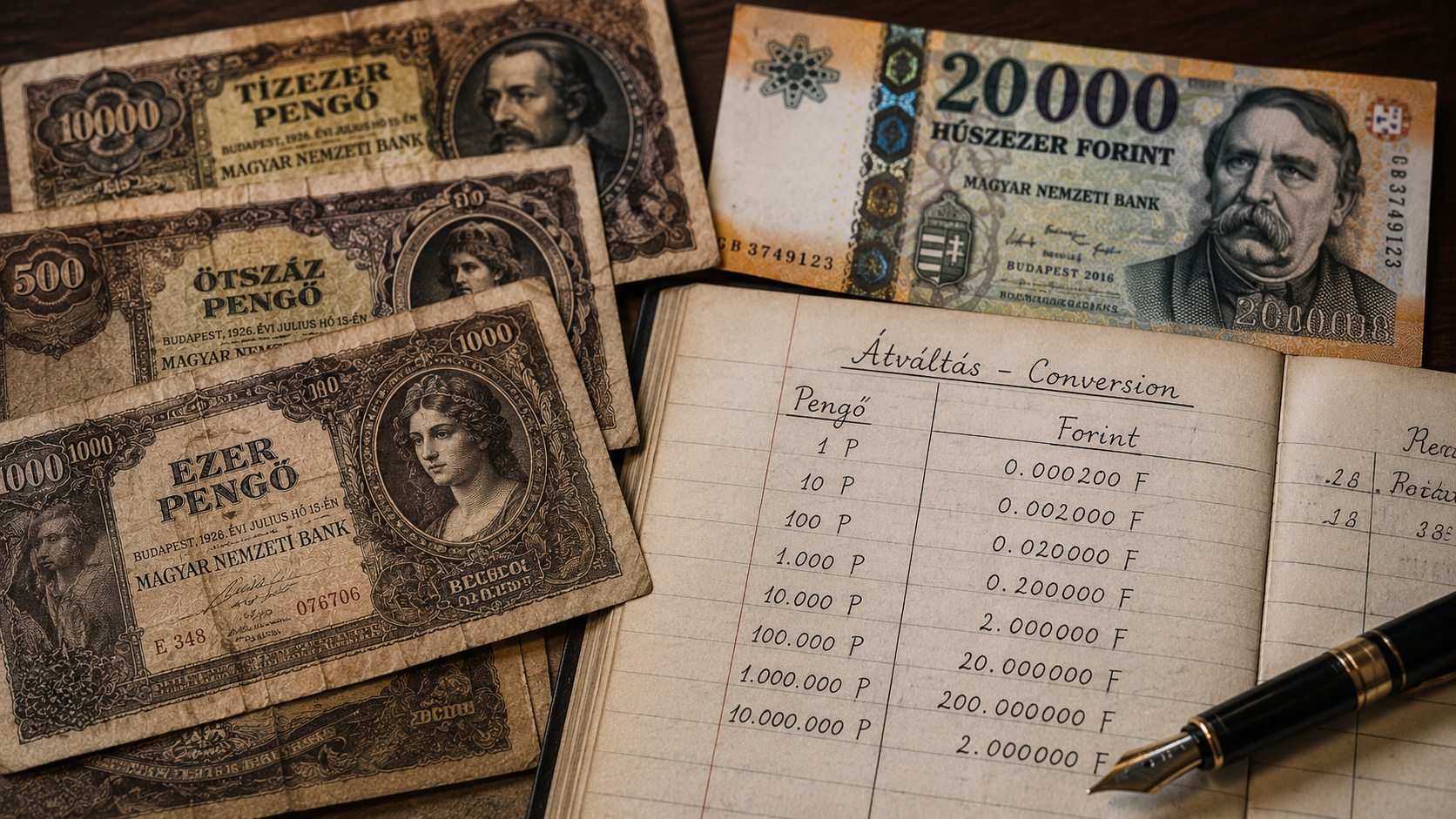

Hungary 1946: The Currency That Could Not Be Saved

Hungary, after the Second World War, faced one of the most extreme monetary collapses recorded. The country had physical destruction, reparations pressure and a state trying to finance obligations by creating money. The pengo became unusable because the unit of account itself had disintegrated.

At that point, reform could not mean rebranding the old currency. It required replacement. Hungary introduced the forint in 1946. Britannica records the conversion from pengo to forint at 400 quintillion to one. That number is almost impossible to process, which is precisely the point: once the zeros become absurd, money has lost its social function.

The new Hungarian Forint worked because it provided a clean accounting break. A destroyed currency carries memory. Every note reminds people of theft by inflation. By replacing the unit, Hungary separated the future price system from the collapsed past.

This is why many hyperinflations do not truly end with a gradual return to normal. They end with institutional rupture. The old money is abandoned, redenominated or replaced because society needs a new measuring stick.

Bolivia 1985: The Budget Had to Be Fixed First

Bolivia shows the side of hyperinflation that is less visually famous than wheelbarrows of cash but more useful for modern policy. By 1985, inflation had become a symptom of a broader state financing crisis. The country faced weak fiscal capacity, external debt pressure and a system in which money creation filled the gap between government promises and government resources.

The New Economic Policy announced in August 1985 attacked the fiscal and monetary causes together. It did not merely introduce a fresh note. It restructured the behaviour of the state. Public spending was cut, prices were liberalised, the exchange-rate policy was reset, and the government moved to stop the deficit from being financed through the printing press.

NBER work on the Bolivian stabilisation describes how the programme ended the hyperinflation quickly after the new government came into office. That speed is important. Hyperinflation can feel unstoppable when viewed from the street, but it can collapse rapidly when the public sees a credible fiscal regime replace the old one.

The lesson from Bolivia is that monetary reform without fiscal reform is cosmetic. If the state continues to spend money it cannot raise, the new currency inherits the old disease.

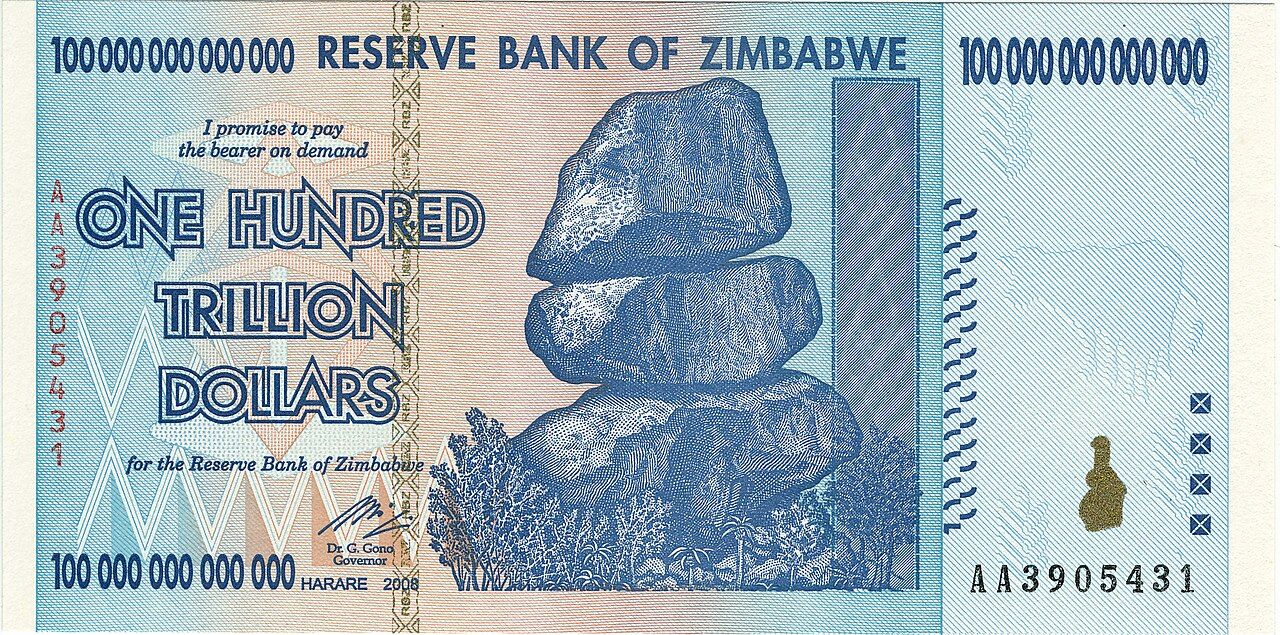

Zimbabwe 2009: Hyperinflation Ended When the Currency Died

Zimbabwe provides a harsher lesson. Sometimes, hyperinflation does not end because a domestic currency is rescued. It ends because the domestic currency is abandoned. By late 2008, economic life had already moved away from the Zimbabwe dollar. People quoted prices in foreign currencies, saved in foreign currencies and judged value through currencies they trusted more.

The IMF stated in 2009 that with the demise of the Zimbabwe dollar, hyperinflation had stopped, and that de facto dollarisation was recognised through the official transition to the use of hard currencies. That line captures the core trade-off. Dollarisation can stabilise prices because the government loses the ability to print the currency people actually use. But it also means the country loses monetary sovereignty.

That loss matters. A dollarised economy cannot run an independent domestic monetary policy in the same way. It becomes dependent on access to foreign currency, export earnings, remittances and external liquidity. Price stability may return, but the deeper institutional wound remains.

Zimbabwe, therefore, shows the difference between stopping hyperinflation and rebuilding monetary credibility. The first can happen through abandonment. The second takes much longer.

The Four Forces That Actually End Hyperinflation

1. A hard stop to deficit financing

The first requirement is a credible stop to monetary financing. If the public believes the government will keep printing to pay wages, subsidies, debt service or military costs, inflation expectations will not stabilise. A new currency can fail immediately if the budget still relies on the central bank.

2. A believable anchor

The second requirement is an anchor that people understand. This may be a new currency with strict issue limits, foreign currency use, gold or asset backing, an exchange-rate rule, central bank independence, or an IMF-supported stabilisation programme. The form matters less than credibility. The public must believe the anchor restricts the government.

3. Political authority

The third requirement is political authority. Hyperinflation is often accompanied by weak institutions, social conflict and a state that cannot enforce a coherent programme. A reform that is technically elegant but politically impossible will not survive contact with reality.

4. Public memory

The fourth force is memory. People who have lost savings to hyperinflation do not trust easily. This is why dollarisation can persist long after inflation falls. It is also why a new currency can struggle even when macroeconomic numbers look better. Trust is rebuilt through repeated restraint, not speeches.

Why Redenomination Alone Fails

A common mistake is to confuse removing zeros with restoring value. Redenomination can make accounting easier. It can help cash registers, invoices and payroll systems function again. But if the government removes six zeros today and prints them back tomorrow, the reform is theatre.

Hyperinflation ends only when a new unit is protected by new rules. This is why some currency reforms succeed, and others merely delay the next collapse. The public judges reform through behaviour: whether deficits fall, whether central-bank financing stops, whether the exchange rate stabilises, whether shops are willing to price in the new money, and whether people are willing to save in it.

This is also why foreign currency often becomes the real referendum. When people can choose, they reveal which money they trust. If they keep wages, contracts and savings in dollars while using local currency only because the law requires it, the domestic monetary system has not fully recovered.

What This Means Today

Inflation control is ultimately institutional

Modern inflation rarely reaches hyperinflationary levels in advanced economies because institutions are stronger, tax systems are deeper and central banks usually have more credibility. But the historical warning remains relevant. Inflation becomes dangerous when fiscal policy, monetary policy and political incentives begin to point in the same inflationary direction.

Debt matters when governments cannot finance it honestly

High debt does not automatically create hyperinflation. The danger comes when a government cannot tax, borrow or cut spending and therefore leans on money creation. Hyperinflation is the end of fiscal dishonesty: a hidden default imposed on anyone holding the currency.

Trust is harder to rebuild than prices are to stabilise

The most important modern lesson is that price stability is only the first stage of recovery. People who have experienced a currency collapse remember it. They diversify into foreign currency, land, gold, property or other real assets. That behaviour can persist for decades.

The modern parallel is not panic - it is discipline

The lesson is not that every inflation spike is Weimar Germany. That comparison is usually lazy. The real lesson is more precise: money depends on institutional limits. When governments respect those limits, inflation can be managed. When they destroy those limits, money becomes a promise nobody believes.

Frequently Asked Questions

What caused the collapse of hyperinflation?

Hyperinflation collapsed when governments stopped the mechanism that created it: financing public spending through money creation. Successful cases usually combined fiscal reform, a credible monetary anchor, and a new or restructured currency that people believed would be limited.

Can hyperinflation end without a new currency?

It can, but the existing currency must be tied to credible constraints. In many historical cases, the old currency was too discredited to save, so governments replaced it, redenominated it, or abandoned it in favour of foreign currencies.

Why did the Rentenmark stop German hyperinflation?

The Rentenmark worked because it was introduced in limited quantities and represented a clear break from uncontrolled paper-mark issuance. It’s backed by industrial and agricultural mortgages, which helped create a believable anchor, but the deeper factor was the end of unlimited money creation.

Why did Zimbabwe’s hyperinflation stop?

Zimbabwe’s hyperinflation stopped after the Zimbabwe dollar effectively died, and foreign currencies became the practical money of the economy. The IMF described the demise of the Zimbabwe dollar and the official use of hard currencies in early 2009 as ending the hyperinflation.

Is hyperinflation the same as high inflation?

No. High inflation can be painful but still manageable within normal monetary systems. Hyperinflation refers to an extreme and accelerating collapse, commonly defined as prices rising by more than 50% per month.

Does printing money always cause hyperinflation?

Not always. Money creation becomes hyperinflationary when it finances persistent fiscal deficits in a context where public confidence has collapsed and productive capacity or foreign-exchange credibility is weak.

What is the main modern lesson from hyperinflation?

The main lesson is that money is an institution, not just paper or digital balances. It depends on fiscal discipline, credible limits, and public belief that the government will not use inflation as a hidden tax.