Hyperinflation is not just a story about worthless banknotes; it is a story about what happens when trust becomes impossible to price. That is why hyperinflation still matters today. It shows how quickly money can stop acting like money when governments, central banks, markets and households no longer believe the same promise: that a currency will hold enough value tomorrow to make exchange possible today.

The danger is not simply that prices rise. Ordinary inflation hurts purchasing power, but hyperinflation breaks the unit of account itself. Wages lose meaning. Contracts become fiction. Savings are destroyed. Shops rewrite prices faster than families can spend their wages. The state may still issue money, but society quietly moves to something else: dollars, gold, goods, favours, foreign currency, or barter. When we study hyperinflation, we are really studying the collapse of monetary credibility.

Why Hyperinflation Still Matters Today

Hyperinflation still matters today because it reveals the point at which inflation stops being a price problem and becomes a trust problem. Economists often use Phillip Cagan's definition: hyperinflation begins when prices rise by more than 50% in a single month. At that speed, the public stops treating money as a store of value and begins spending, exchanging or converting it as quickly as possible.

The modern lesson is direct. Countries do not need wheelbarrows of banknotes to suffer the early warning signs. Fiscal dominance, weak institutions, political pressure on central banks, uncontrolled money creation, supply shocks, exchange-rate collapse and unanchored inflation expectations can all push an economy towards monetary disorder. Hyperinflation matters because it shows what happens when policy credibility is lost before the currency is formally abandoned.

The most important point is that hyperinflation is rarely solved by printing a larger note. It ends when a government creates a credible new anchor: a reformed currency, hard fiscal limits, external support, independent monetary control, or the practical adoption of a trusted foreign currency. That is why the subject remains relevant for investors, policymakers and ordinary households watching inflation, public debt and central bank credibility today.

The Night Money Lost Its Meaning

The speed of collapse matters

In a normal inflationary period, people complain that money buys less each month. In hyperinflation, they behave as if money is melting in their hands. The shift is behavioural before it is technical. A shopkeeper does not wait for the official statistics. A worker does not need a central bank report to know that wages are becoming useless by payday. The market moves first, and official recognition arrives later.

This is why the 50% per month definition is useful but incomplete. It gives us a clean threshold, but hyperinflation becomes visible in daily behaviour: wages paid more frequently, prices quoted in foreign currency, landlords refusing long fixed contracts, businesses holding inventory instead of cash, and households converting local money into food, fuel or durable goods.

The monetary system depends on delay. You accept money today because you believe someone else will accept it tomorrow. Hyperinflation destroys that delay. Everyone tries to spend before everyone else. The currency then loses one of its core functions: storing value across time.

The story is always about credibility

The same pattern appears across very different countries. The technical causes vary - war finance, reparations, fiscal deficits, central bank accommodation, supply collapse, sanctions, political instability, exchange-rate pressure - but the deeper mechanism is credibility loss.

Once the public believes that the government will meet obligations by creating money rather than by collecting revenue, cutting expenditure, restructuring debt or restoring production, the currency becomes a political liability. Prices then stop reflecting only supply and demand. They begin to reflect fear about tomorrow's policy decisions.

That is the storytelling thread running through Weimar Germany, Hungary after the Second World War and Zimbabwe in the 2000s. In each case, the currency did not collapse because people forgot how to count. It collapsed because the public no longer believed the institutions behind the money.

Weimar Germany: The Warning That Still Defines Hyperinflation

A post-war state under impossible pressure

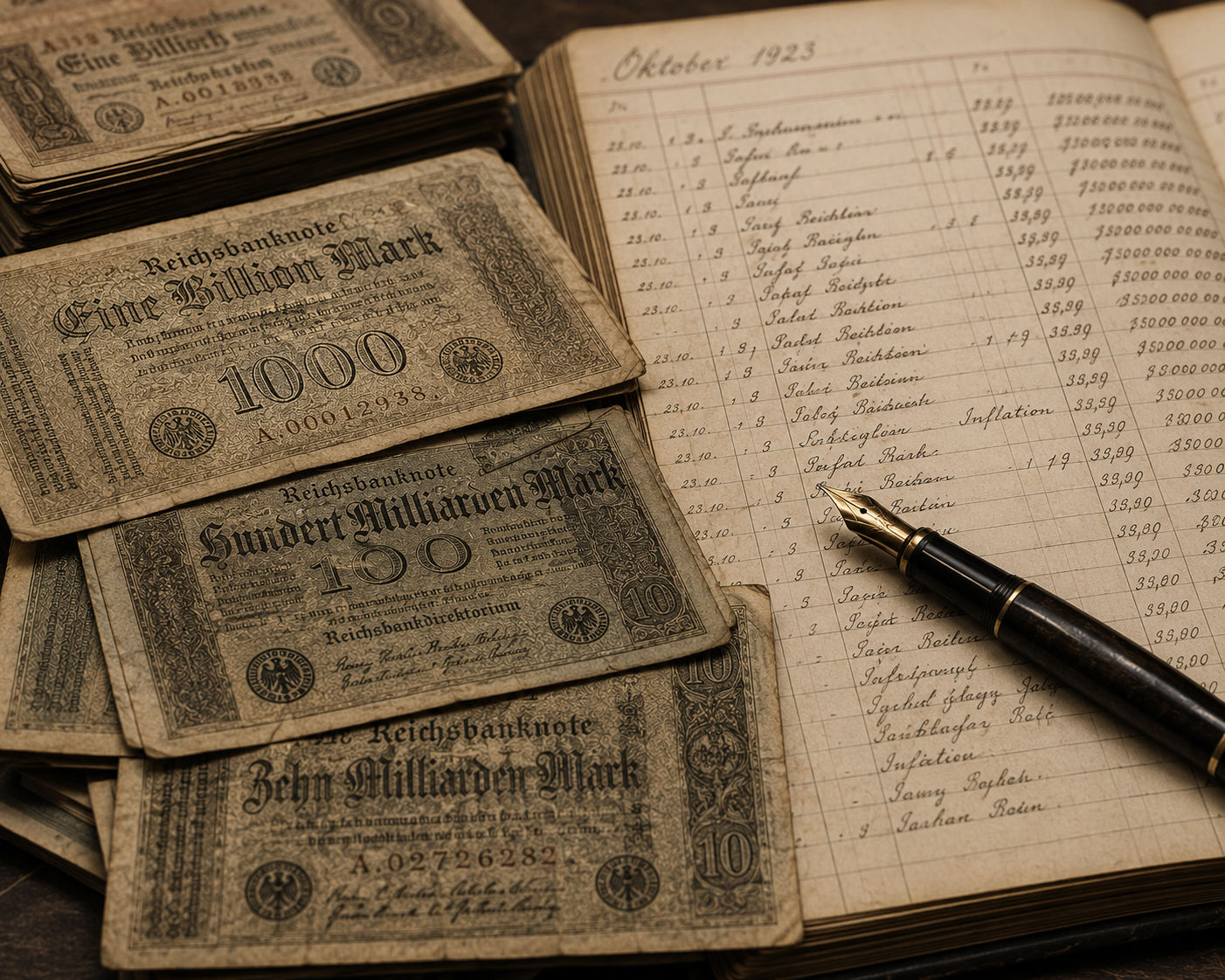

The Weimar Republic did not enter the 1920s with a calm balance sheet. Germany had financed much of the First World War through borrowing rather than taxation, then faced reparations and political fragility after defeat. The state needed money, the economy was strained, and the mark became the pressure valve.

The famous images of people carrying notes in baskets are memorable because they make monetary collapse visible. But the deeper story is more important. Weimar hyperinflation changed the relationship between citizens and the state. Middle-class savers who had behaved prudently saw lifetime savings disappear. Pensioners discovered that fixed incomes could be destroyed without a formal default. Debtors gained, creditors lost, and trust in moderate institutions weakened.

By November 1923, the exchange rate had reached the point where one US dollar was worth trillions of paper marks. The currency had become a symbol of state failure rather than national value. A society that had once treated the mark as ordinary money began treating it as a wasting asset.

Why Weimar still shapes modern inflation fear

Weimar matters today because it taught generations that inflation can become political. It did not automatically create the later catastrophe of German politics, but it helped undermine the social centre. People who lose savings, pensions and contracts do not experience inflation as an abstract economic variable. They experience it as betrayal.

Modern advanced economies are not Weimar Germany. They have deeper capital markets, independent central banks, broader tax systems and more resilient institutions. But the Weimar lesson remains alive because it sits inside public memory: when money loses credibility, democratic legitimacy can also weaken.

That is why policymakers watch inflation expectations so closely. The fear is not simply that prices rise for one year. The fear is that households and firms begin to build future inflation into wage demands, contracts, rents and pricing decisions. Once that mindset hardens, reversing it becomes more painful.

Hungary 1946: The Most Extreme Monetary Collapse on Record

When prices doubled within hours

Hungary's post-war hyperinflation was even more extreme than Weimar's. After the Second World War, Hungary faced destruction of productive capacity, fiscal stress and monetary chaos. The pengo collapsed at a speed that makes ordinary inflation language almost useless. Guinness World Records records Hungary's July 1946 inflation at 41.9 quadrillion per cent for the month, with prices doubling roughly every 15 hours.

This matters because Hungary shows the mathematical violence of compounding. A price rise that sounds impossible becomes mechanically possible when confidence disappears, and money supply growth accelerates into a broken economy. At that point, the banknote denomination becomes theatre. Larger notes do not restore value; they merely document the collapse.

Hungary eventually stabilised through currency reform, introducing the forint in August 1946. The lesson is direct: hyperinflation ends only when people believe the new unit is tied to a credible fiscal and monetary regime. A currency reform without discipline is a name change. A currency reform with discipline can rebuild the unit of account.

The human cost behind the numbers

Extreme inflation statistics can become absurdly large, which makes them feel detached from real life. That is dangerous. Behind every figure sits a transfer of wealth. Cash holders lose. Fixed-income households lose. Savers lose. Wage earners lose unless pay adjusts instantly. People with hard assets, foreign currency or politically protected access to goods are more likely to survive.

Hyperinflation, therefore, redistributes wealth before anyone votes on redistribution. It punishes the cautious and rewards those who are already positioned outside the collapsing currency. This is one reason it still matters today. Inflation is never only a macroeconomic chart; it is a social allocation mechanism.

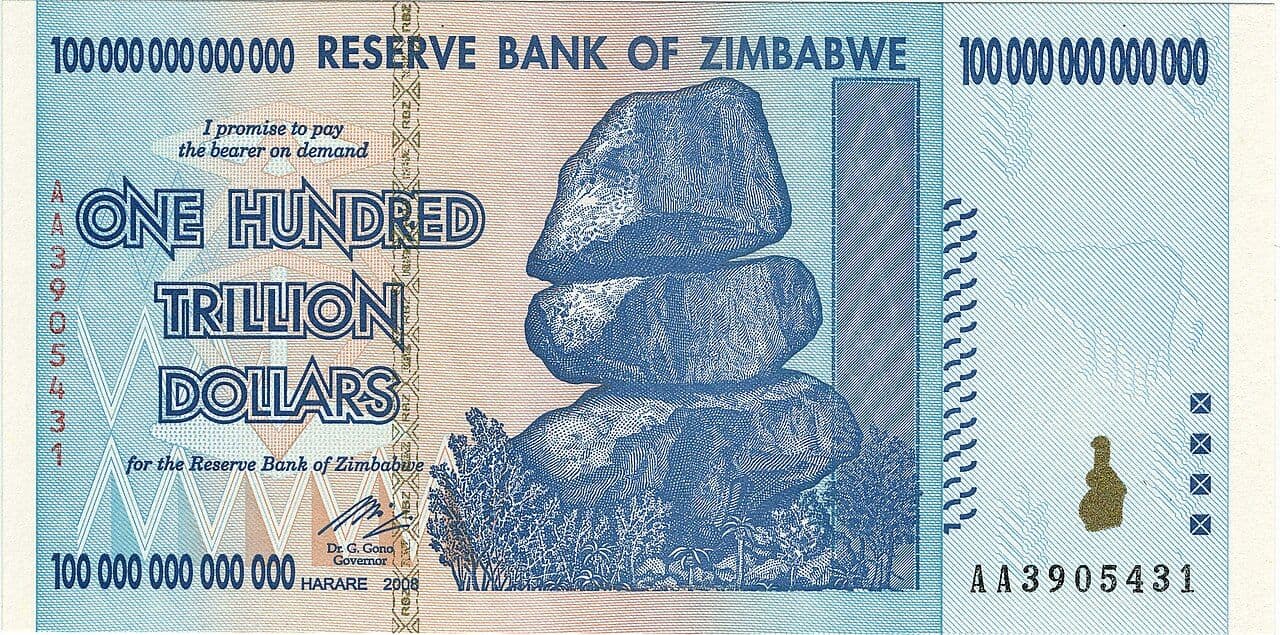

Zimbabwe: The Modern Case of Currency Rejection

A currency can die before it is officially buried

Zimbabwe's hyperinflation showed a modern economy moving away from its own currency in real time. By the late 2000s, the Zimbabwe dollar had lost practical credibility. Shops, households and businesses increasingly relied on foreign currencies because the local unit could not perform the basic functions of money.

The IMF noted in 2009 that with the demise of the Zimbabwe dollar, hyperinflation had stopped, and that official recognition of hard currencies reflected the de facto dollarisation already taking place. This is a crucial phrase: de facto first, official recognition second. Citizens and markets had already made the monetary decision before the state fully acknowledged it.

That is one of the most important modern lessons. A government can print a currency, but it cannot force trust at scale. Legal tender status matters, but it cannot make people save in a currency they believe will collapse.

Dollarisation solves one problem and creates another

Zimbabwe's dollarisation helped stabilise prices because it imported monetary credibility. The US dollar gave households and businesses a unit they trusted more than the domestic currency. But this came at a cost: the country surrendered a large part of its monetary sovereignty.

That trade-off matters today because it reveals the endgame of currency failure. When a domestic currency dies, the replacement anchor often comes from outside: the dollar, the euro, gold, a currency board, or an externally supported stabilisation programme. Stability returns, but policy flexibility shrinks.

For ordinary people, the choice is not theoretical. They choose the money that works. If their salaries, rents, savings and business costs are safer in a foreign currency, they will use it even when politicians insist the local currency should be enough.

The Mechanism: How Inflation Turns Into Hyperinflation

Fiscal dominance comes first

Hyperinflation is often described as a central bank failure, but the fiscal story usually sits underneath it. A government spends more than it can sustainably finance. If borrowing options narrow and taxation cannot close the gap, the temptation grows to use money creation as a funding tool. The central bank then becomes a fiscal instrument.

This is the danger economists call fiscal dominance. Monetary policy no longer leads. It follows the needs of the state. Interest rates, liquidity provision and money creation become shaped by the government's financing position rather than the currency's stability.

Modern economies can face versions of this pressure without entering hyperinflation. High debt, political pressure for cheap borrowing, emergency spending and resistance to fiscal consolidation can all test the boundary between monetary independence and fiscal convenience. The lesson from hyperinflation is that once markets believe the boundary has disappeared, the currency revalues quickly.

Expectations convert pressure into panic

Inflation expectations are the bridge between policy and behaviour. If households expect prices to rise sharply, they spend sooner. If firms expect costs to rise, they increase prices faster. If workers expect purchasing power to fall, they demand higher wages. If lenders expect repayment in weaker money, they charge more or refuse long-term contracts.

This feedback loop does not require everyone to understand macroeconomics. It only requires people to protect themselves. Hyperinflation begins when protection behaviour becomes universal.

That is why central bank credibility is valuable. Credible institutions can slow the feedback loop because the public believes policy will eventually restore price stability. Weak institutions accelerate the loop because every official assurance sounds temporary.

Exchange rates become the public scoreboard

In many hyperinflationary episodes, the exchange rate becomes the most important daily indicator. People stop asking what the official inflation rate is and start asking what the local currency buys against the dollar, gold or another trusted reference.

This matters because an exchange-rate collapse can feed domestic prices. Imports become more expensive. Businesses using foreign inputs raise prices. Households convert savings faster. The exchange rate becomes both a symptom and a driver of the crisis.

For modern economies, this is why currency credibility remains central. A country can tolerate temporary inflation. It struggles when the public believes the domestic currency itself is no longer a credible claim on future purchasing power.

Why Hyperinflation Still Matters for Investors and Households

It changes how we think about cash

Cash is usually treated as a safety net. Hyperinflation reverses that assumption. In a monetary collapse, cash becomes the risk asset because its purchasing power falls fastest. The safest position is no longer the most liquid domestic asset; it may be foreign currency, inflation-linked income, hard assets, productive business ownership or claims tied to external markets.

This does not mean households in stable economies should behave as if hyperinflation is imminent. That would be poor analysis. It means we should understand cash risk properly. Money is safe only when the institution behind it is credible.

It exposes the difference between nominal wealth and real wealth

Hyperinflation teaches a brutal lesson: a larger number is not the same as greater wealth. A salary can rise every week while living standards collapse. A bank balance can contain more zeros while buying less food. Government debt can be repaid in nominal terms, while creditors are destroyed in real terms.

This distinction matters in any inflationary period. We should ask not only whether income, asset values or revenues are rising, but whether they are rising faster than the cost of maintaining real purchasing power.

The wealthy often survive inflation better because they hold assets that reprice. The vulnerable often hold cash wages, fixed pensions or domestic savings. Hyperinflation widens that divide dramatically.

It reminds us that trust is an economic asset

Trust sounds soft, but in monetary systems, it is hard infrastructure. It lowers transaction costs. It allows long contracts. It supports credit. It lets wages be paid monthly rather than daily. It lets people save in the domestic currency instead of constantly searching for an exit.

When trust fails, the economy becomes shorter-term. Contracts shorten. Investment falls. Foreign currency dominates. Political anger rises. The state may still function, but every transaction carries a credibility discount.

That is why hyperinflation still matters today, even in countries far from the edge. It is the extreme case that reveals what normal money quietly depends on.

The Warning Signs Modern Economies Should Watch

The first warning is not a large banknote

By the time a country prints absurdly large banknotes, the crisis is already advanced. The earlier warning signs are more subtle: persistent fiscal deficits funded through monetary accommodation, political attacks on central bank independence, capital flight, widening black-market exchange rates, indexation of wages and rents, refusal to hold long-term local-currency contracts, and public preference for foreign currency.

These signals matter because hyperinflation is cumulative. It is not a switch that flips overnight. It is a sequence in which policy weakness becomes credibility loss, credibility loss becomes behavioural change, and behavioural change becomes a self-reinforcing price spiral.

The second warning is institutional denial

Another common warning sign is denial. Governments often blame speculators, foreign enemies, greedy merchants or temporary shocks. Sometimes those factors play a role, but they do not explain sustained currency collapse on their own.

When officials refuse to address fiscal imbalance, monetary expansion and confidence loss, the public learns to ignore official explanations. That makes the crisis harder to stop. Stabilisation requires policy credibility, and credibility is not rebuilt by insisting that reality is temporary.

What This Means Today

Inflation is manageable while trust remains anchored

The modern world has not escaped inflation risk. Supply shocks, geopolitical conflict, energy volatility, high public debt and political pressure on central banks all matter. But the line between inflation and hyperinflation is still credibility.

A country with credible institutions can suffer high inflation and recover. A country without credibility can see smaller shocks become destabilising because households and markets assume policymakers will choose the politically easier path over the monetary anchor.

This is why inflation expectations receive so much attention. They are not just forecasts. They are evidence of whether the public still believes the monetary regime.

Central bank independence is not an academic detail

Central bank independence matters because it separates the currency from short-term political financing. When that separation weakens, markets begin to ask whether money creation will be used to solve fiscal problems. Hyperinflation is the extreme version of that fear.

The lesson is not that elected governments should have no role in economic policy. The lesson is that monetary credibility needs institutional protection. Once a central bank becomes visibly subordinate to fiscal pressure, the currency may start carrying a political risk premium.

The final lesson is simple: money is a promise

Every currency is a promise backed by law, taxation, productive capacity, institutional competence and public belief. Hyperinflation is what happens when that promise breaks. It still matters today because it reminds us that monetary stability is not automatic. It is built, defended and sometimes lost.

For readers of Coin & Empire, the central lesson is clear. Follow the money, and you will usually find the deeper story: who holds power, who absorbs losses, who escapes the currency, and who pays the price when trust disappears.

Frequently Asked Questions

What is hyperinflation?

Hyperinflation is an extreme form of inflation where prices rise so quickly that the currency stops functioning properly as money. Economists often use the threshold of more than 50% inflation in a single month.

Why does hyperinflation happen?

Hyperinflation usually happens when fiscal crisis, excessive money creation, weak production, political instability and collapsing confidence reinforce each other. It is not just high inflation; it is a breakdown in monetary credibility.

Why is Weimar Germany important to hyperinflation history?

Weimar Germany is important because its 1921-1923 inflation destroyed savings, weakened the middle class and became one of the most famous examples of money losing public trust. It remains a reference point for modern inflation fear.

Which country had the worst hyperinflation?

Hungary recorded the most extreme known hyperinflation in July 1946, when prices doubled about every 15 hours and monthly inflation reached 41.9 quadrillion per cent.

Can hyperinflation happen in advanced economies?

It is much less likely in advanced economies with independent central banks, deep tax systems and credible institutions. But the lesson still matters because credibility, fiscal discipline and inflation expectations can weaken in any monetary system.

How does hyperinflation end?

Hyperinflation ends when a credible monetary anchor is restored. That can involve a new currency, fiscal reform, central bank discipline, external support, currency boards, dollarisation or a combination of these measures.

Why should investors care about hyperinflation?

Investors should care because hyperinflation exposes the difference between nominal wealth and real wealth. It shows why currency risk, inflation protection, asset quality and institutional credibility matter.