The most dangerous price crisis of the twentieth century was not caused by prices rising too fast, but by prices falling too far. That is why the Great Depression inflation story matters. It forces us to look beyond the familiar fear of rising prices and study the opposite threat: deflation, collapsing money, debt pressure and a loss of confidence so severe that households stopped spending, banks stopped lending, and businesses stopped investing. Inflation is usually treated as the villain of economic history. The 1930s show a harder truth. When policymakers crush demand, protect monetary rules at the wrong moment or allow money to disappear from the system, falling prices can become just as destructive as runaway inflation.

Quick Answer: What Does The Great Depression Teach Us About Inflation?

The Great Depression teaches us that price stability is not the same as permanently low inflation at any cost. Between 1929 and 1933, the United States suffered a severe contraction: real GDP fell sharply, unemployment surged, consumer prices fell by roughly a quarter, wholesale prices fell even more, and thousands of banks failed. The lesson is not that inflation should be tolerated without limit. The lesson is that a collapsing money supply and falling prices can turn a recession into a systemic crisis.

Inflation becomes dangerous when it destroys trust in money. Deflation becomes dangerous when it makes every debt harder to repay. The 1930s demonstrate that central banks and governments must prevent both extremes. Stable money requires credibility, but it also requires flexibility. A rigid defence of gold convertibility, tight money and delayed bank stabilisation made the Depression deeper than it needed to be.

For modern readers, the central lesson is practical: inflation policy is not only about raising or cutting interest rates. It is about protecting the monetary plumbing beneath the economy. If banks fail, credit contracts and households expect prices to keep falling, even low inflation can become a crisis signal rather than a success.

The Price Crisis Began Before People Understood It

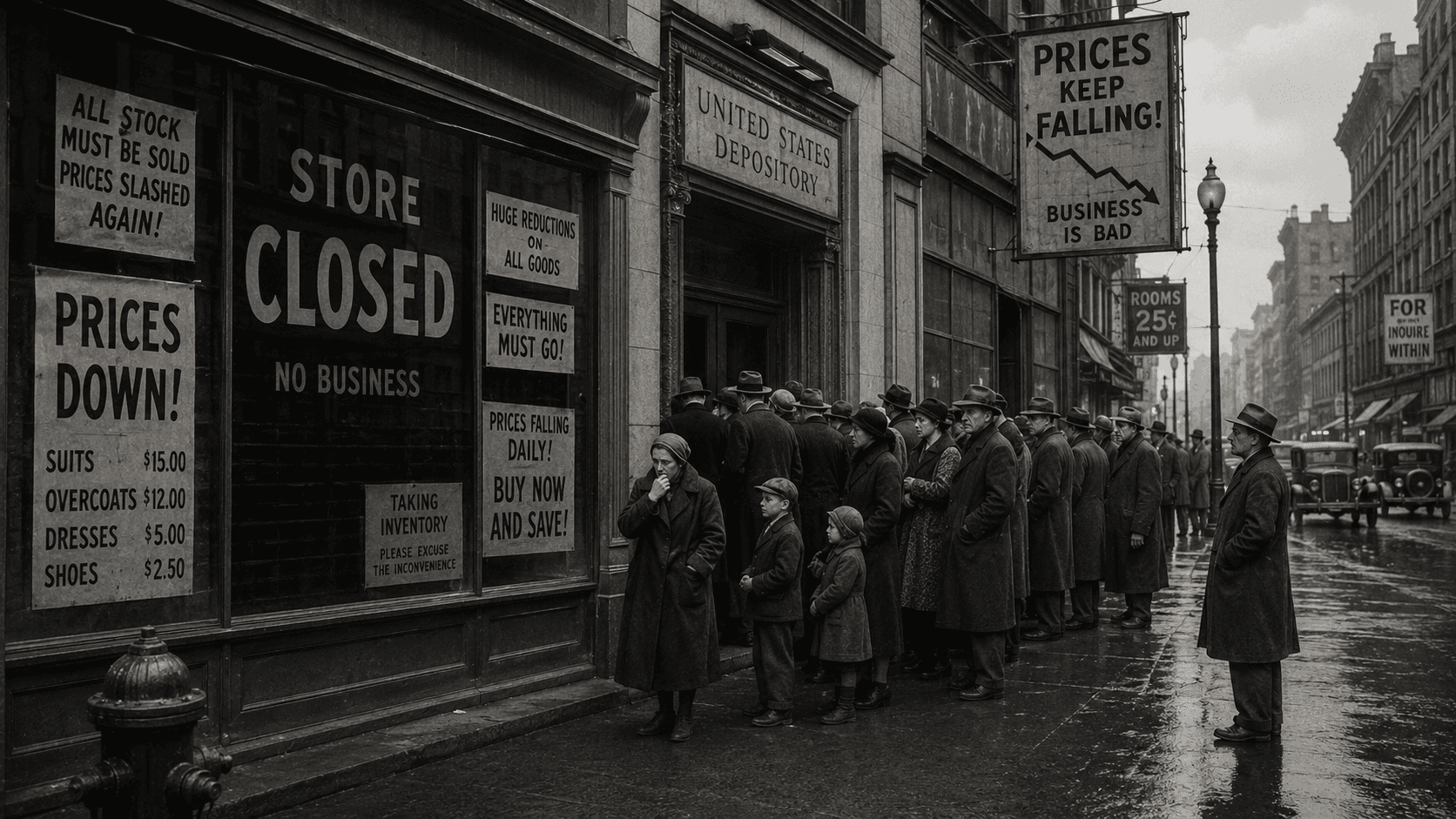

In 1929, the American economy looked rich on the surface. Share prices had risen dramatically, consumer credit was expanding, and factories were producing for a society that believed prosperity had become permanent. Then the financial story changed. The stock market crash did not immediately explain the full Depression, but it exposed how fragile confidence had become. When asset prices fell, households and firms pulled back. When spending weakened, businesses cut production. When businesses cut production, workers lost income. The cycle fed itself.

The first inflation lesson comes from that sequence. Price movements are not isolated numbers. They are signals inside a wider credit system. Once confidence broke, the fall in prices did not feel like relief to ordinary people. Cheaper goods mattered little if wages were falling, jobs were disappearing, and banks were no longer safe places to keep savings.

Deflation made debt heavier

A household with a fixed mortgage, a farmer with a bank loan or a business with bonds outstanding did not see their debt fall when prices fell. Their nominal obligations stayed the same while incomes and sale prices dropped. This is the debt-deflation trap. Each fall in prices raised the real burden of past borrowing. The more borrowers tried to sell assets and cut costs, the more pressure they placed on prices.

That is why the Depression teaches us that low prices are not automatically good prices. If wages, incomes and asset values are falling together, cheaper goods can arrive alongside higher real debt and mass insolvency. A price index may show deflation, but the lived economy feels like suffocation.

The Depression Was A Deflationary Inflation Lesson

The phrase “Great Depression inflation” can sound contradictory because the Depression was not a classic inflationary episode. It was a deflationary collapse. Yet that is exactly why it teaches us so much about inflation. Inflation policy is about the value of money over time. Deflation is the same problem in reverse: money becomes more valuable relative to goods, but only because the economy is shrinking around it.

In ordinary life, falling prices sound attractive. In a depression, falling prices become a warning that buyers are absent, incomes are weak, and firms have lost pricing power. A shopkeeper can mark goods down. A factory can cut wages. A farmer can sell crops for less. But debts, rents and many contractual obligations do not adjust as quickly. That gap between falling income and fixed obligations is where economic damage compounds.

The money supply mattered as much as the price index

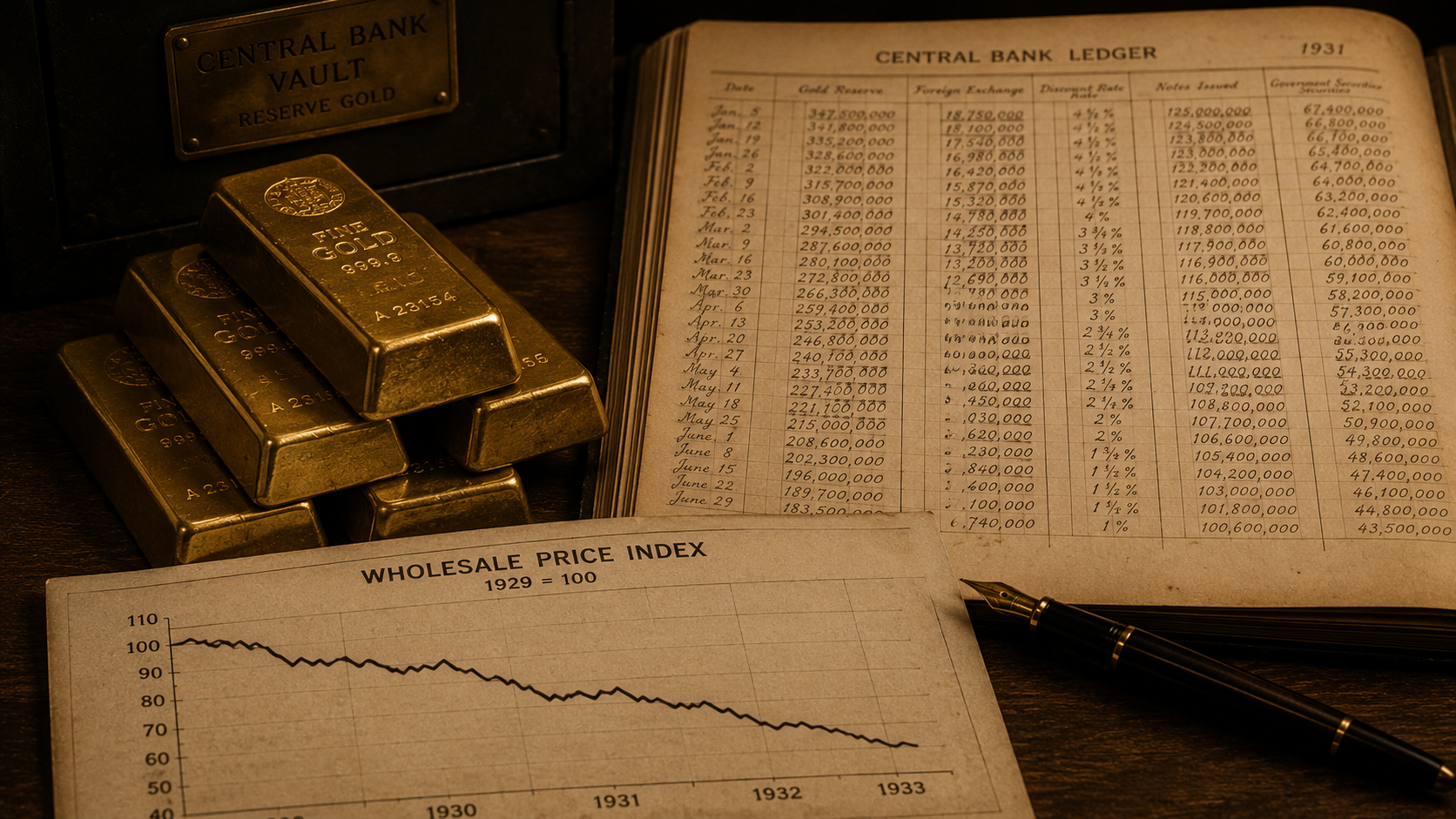

From late 1930 to early 1933, the U.S. money supply fell by nearly 30 per cent, according to Federal Reserve History. That contraction was not a minor technical detail. Money is the settlement layer of the economy. When banks fail, and deposits disappear, households become more cautious, firms delay investment, and lenders become defensive. Prices then fall not because production has become more efficient, but because the economy has lost spending power.

This is where the Depression still speaks to modern inflation debates. Price stability cannot be judged only by today’s inflation rate. We also need to ask whether credit is available, whether deposits are trusted, whether wages are stable and whether expectations are anchored. In the 1930s, the official price movement was downward, but the underlying system was failing.

Gold Made The Policy Mistake Harder To Escape

The gold standard gave money a promise: currency could be converted into a fixed quantity of gold. In stable times, that promise helped create credibility. In the early 1930s, it became a constraint. Governments and central banks feared that expansionary policy would weaken confidence in convertibility. Instead of acting aggressively to stop deflation, they often defended gold parity, even as output, employment and banks deteriorated.

This is one of the most important lessons for inflation policy. A monetary rule can create discipline, but if the rule prevents action during a financial collapse, discipline becomes fragility. The problem was not gold as a metal. The problem was the political and institutional commitment to a fixed monetary arrangement at the wrong moment.

Leaving gold changed expectations

Research on the Depression repeatedly shows that countries which left the gold standard recovered earlier than countries that remained tied to it. That did not happen because abandoning gold magically created prosperity. It happened because it changed expectations. Once governments could expand money, support banks and stop forcing internal deflation, households and firms had a reason to believe prices and incomes would stop falling.

Inflation expectations matter because economies are forward-looking. If people expect lower prices tomorrow, they delay spending today. If firms expect weak demand, they postpone hiring and investment. If borrowers expect incomes to fall, they hoard cash. A credible shift away from deflation can therefore stimulate activity before every policy measure has fully worked through the economy.

Bank Failures Turned Price Pressure Into A Trust Crisis

Inflation and deflation both become more dangerous when people stop trusting financial institutions. During the Depression, bank failures did not merely inconvenience depositors. They destroyed money balances, froze credit relationships and convinced households that the safest action was to withdraw or hoard cash. That defensive behaviour made the contraction worse.

The FDIC records show the 1930s as a decade defined by banking stress. Deposit insurance was created in response to that experience because policymakers learned that monetary stability depends on public trust. If depositors believe their money is unsafe, even a solvent banking system can come under pressure. If thousands of banks fail, the public does not distinguish between technical liquidity problems and permanent loss. It simply retreats.

Deposit insurance was an inflation lesson as well as a banking reform

Deposit insurance is usually discussed as a banking reform, but it also belongs within the inflation story. A modern economy uses bank deposits as money. When people believe deposits are safe, payments continue, loans can be made and ordinary commerce moves. When deposits are feared, the money supply can contract even if the central bank has not deliberately chosen deflation.

That is why the New Deal banking reforms were not separate from the fight against the Depression. They were part of the machinery that helped restore monetary confidence. Stable prices need stable institutions. A central bank cannot manage inflation effectively if the public is simultaneously questioning whether bank money is safe.

The Human Story: Falling Prices Did Not Feel Like Relief

The strongest way to understand the Depression is through the person trapped inside the numbers. Imagine a farmer in 1932. Crop prices have fallen. The bank wants payment. The family still needs equipment, seed and food. Selling more produce does not solve the problem if every bushel earns less than before. Now imagine a shop worker whose employer cuts hours because customers are waiting for lower prices. The price decline that looks helpful on paper becomes the mechanism through which income disappears.

This is the point modern inflation debates often miss. People care about purchasing power, not inflation in isolation. If prices rise by 5 per cent but wages rise by 7 per cent, the experience differs from prices falling by 5 per cent while wages fall by 20 per cent and employment disappears. The Depression teaches us to judge price movements through incomes, debt and employment.

Expectations can trap an economy

Once deflation becomes expected, it changes behaviour. Buyers delay purchases. Businesses run down inventories. Banks tighten standards. Workers accept lower wages or lose jobs. Governments collect less tax revenue. Each defensive decision makes sense individually, but together they push the economy deeper into contraction. Inflation expectations work the other way when they become unanchored, but the Depression shows that deflationary expectations can be equally corrosive.

The Recovery Started When Policy Stopped Worshipping Price Fall

Recovery from the Depression did not arrive because prices were allowed to fall indefinitely until the market cleared. It began when the policy changed the direction of expectations. Banking stabilisation, fiscal support, monetary expansion and the abandonment of the strict gold constraint all helped convince people that the downward spiral could end.

This matters for modern inflation policy because it separates credibility from rigidity. A credible central bank is not one that always tightens. It understands the problem it is facing. If inflation is driven by excessive demand, loose credit and unanchored expectations, tighter policy may be necessary. If the economy is facing bank failures, falling prices and collapsing demand, the same medicine can become poison.

The best inflation policy is regime awareness

The Depression teaches us to ask what type of price problem we are facing. Is money losing value because demand is overheated? Are prices rising because supply has been damaged? Are prices falling because credit has collapsed? Are inflation expectations unanchored, or are deflation expectations taking hold? The answer determines the policy response.

A single inflation number is never enough. We need to look at wages, output, credit conditions, banking stability, commodity prices, government debt, global trade and expectations. The 1930s were catastrophic, partly because officials treated a structural financial crisis through the lens of monetary orthodoxy for too long.

What The Great Depression Teaches Central Banks Today

Central banks today were shaped by the failure of the 1930s. Modern monetary authorities are expected to protect price stability, but they are also expected to serve as lenders of last resort during financial crises. That dual responsibility is not accidental. It reflects the lesson that money, banking and confidence are inseparable.

The Depression showed that allowing the money supply to contract during a banking crisis can magnify every other weakness in the economy. It also showed that the public’s expectations about future prices can either trap an economy or help release it. When policy is late, unclear or constrained by an obsolete rule, the market fills the silence with fear.

Price stability is a corridor, not a point

Modern inflation targets often sit around low positive inflation because a small buffer helps reduce the risk of outright deflation. The Depression explains why. Zero inflation may sound ideal, but an economy repeatedly flirting with falling prices can become vulnerable when demand weakens. A modest positive target gives policymakers room before debt-deflation dynamics take hold.

That does not mean high inflation is harmless. It means the safest monetary regime is one where inflation is low, positive, predictable and supported by credible institutions. The Depression is not an argument for permanent stimulus. It is an argument against confusing falling prices with healthy money.

What This Means Today

Inflation policy must protect trust, not just hit a number

The Great Depression teaches us that inflation control is ultimately about trust. People must trust that money will not lose value rapidly, but they must also trust that the banking system will not destroy their deposits and that policy makers will not allow a downward spiral to continue in the name of discipline. The credibility that matters is not theatrical toughness. It is the ability to act correctly for the economic regime in front of us.

Debt changes the meaning of price movements

A highly indebted economy experiences deflation differently from a low-debt economy. When households, companies and governments carry large nominal obligations, falling prices can raise real debt burdens quickly. This does not mean inflation should be engineered to erase debt. It means policymakers must recognise that sudden disinflation or deflation can create financial stress if income growth collapses at the same time.

Supply shocks and demand collapses need different responses

Modern inflation can come from energy shocks, supply chain disruption, fiscal stimulus, labour shortages or excessive credit growth. The Depression was different because it involved a collapse of money, demand and banking confidence. The practical lesson is to diagnose the cause before prescribing policy. Raising rates into a supply shock or tightening into a banking panic can transmit pain without solving the underlying problem.

The Depression still defines the central banking playbook

When modern central banks respond quickly to bank runs, provide liquidity or communicate inflation targets, they are working in the shadow of the 1930s. The Depression remains the warning case. It shows what can happen when financial panic, deflation and policy hesitation combine. For investors, households and governments, the message is the same: watch prices, but also watch credit, banks and expectations.

Frequently Asked Questions

Was the Great Depression caused by inflation?

No. The Great Depression was primarily a deflationary crisis, not a high-inflation crisis. Its inflation lesson comes from the opposite danger: prices, wages, output and the money supply fell together, which increased debt burdens and weakened confidence.

Why did prices fall during the Great Depression?

Prices fell because demand collapsed, credit contracted, and the banking system came under severe stress. When households and businesses cut spending at the same time, sellers had to reduce prices, but those lower prices also damaged incomes and debt repayment capacity.

What is debt deflation?

Debt deflation is the process by which falling prices and incomes make fixed debts more expensive in real terms. Borrowers then cut spending or sell assets to service debt, which can push prices down further and deepen the downturn.

How did the gold standard affect inflation during the Depression?

The gold standard restricted the ability of governments and central banks to expand money during the crisis. Countries that left gold earlier generally gained more policy flexibility and recovered sooner than those that stayed tied to the system.

What does the Depression teach us about central banks?

It teaches that central banks must protect both price stability and financial stability. Allowing the money supply to contract during a banking panic can turn a recession into a depression.

Is deflation worse than inflation?

Neither is automatically worse in every situation. High inflation destroys purchasing power and trust in money, while severe deflation increases real debt burdens and can freeze spending. The Depression shows why policymakers try to avoid both extremes.

Why do modern central banks target low positive inflation?

A low positive inflation target creates a buffer against deflation. The Depression showed that falling prices can be dangerous when they coincide with weak demand, bank failures and heavy debt.