In July 1946, the price of a loaf of bread in Hungary doubled every fifteen hours. A Hungarian worker who collected their wages in the morning and waited until evening to spend them would find their salary worth half as much by the time they reached the shops. It was not a question of misfortune or bad luck. It was the arithmetic consequence of a currency system that had completely broken down.

This is what hyperinflation looks like in practice — not the slow erosion of purchasing power that modern central banks manage with interest rate adjustments, but a total and accelerating collapse of confidence in money itself. The economist Philip Cagan defined it as inflation exceeding 50% per month. By that measure, historians have documented 57 confirmed cases since the French Revolution. Every single one shares the same underlying mechanism in the currency system behind hyperinflation: a government that can no longer fund its obligations through taxation or genuine borrowing, and that turns to the printing press as the only available tool.

In this article, we trace that mechanism — its triggers, its stages, its human consequences, and the monetary architecture required to stop it — through the four most instructive cases in modern history.

What Is the Currency System Behind Hyperinflation?

At its core, hyperinflation is a failure of the fiscal-monetary relationship. Modern currency systems operate on trust: citizens accept paper money because they believe the issuing authority will manage its supply responsibly and that it can be exchanged for goods at a predictable price. That trust rests on two pillars — fiscal credibility (the government can pay its debts through taxation) and monetary discipline (the central bank controls money creation independently of political pressure).

When both pillars collapse simultaneously, the mechanism is consistent across every case. The government faces a spending crisis — war, reparations, debt, or political emergency — that it cannot cover through taxes or borrowing at affordable rates. It instructs the central bank to create money to cover the deficit. The money supply expands faster than economic output. Prices rise. As prices rise, the government's own expenditure grows in nominal terms, requiring yet more money creation. The feedback loop accelerates until the currency loses its function as a store of value — and citizens begin to exit it as fast as they can.

Peter Bernholz, who analysed 29 hyperinflationary episodes in Monetary Regimes and Inflation, concluded that at least 25 of the 29 were caused by public deficits financed by money creation. The route varies — war debt, reparations, land collapse, sanctions — but the mechanism is essentially the same.

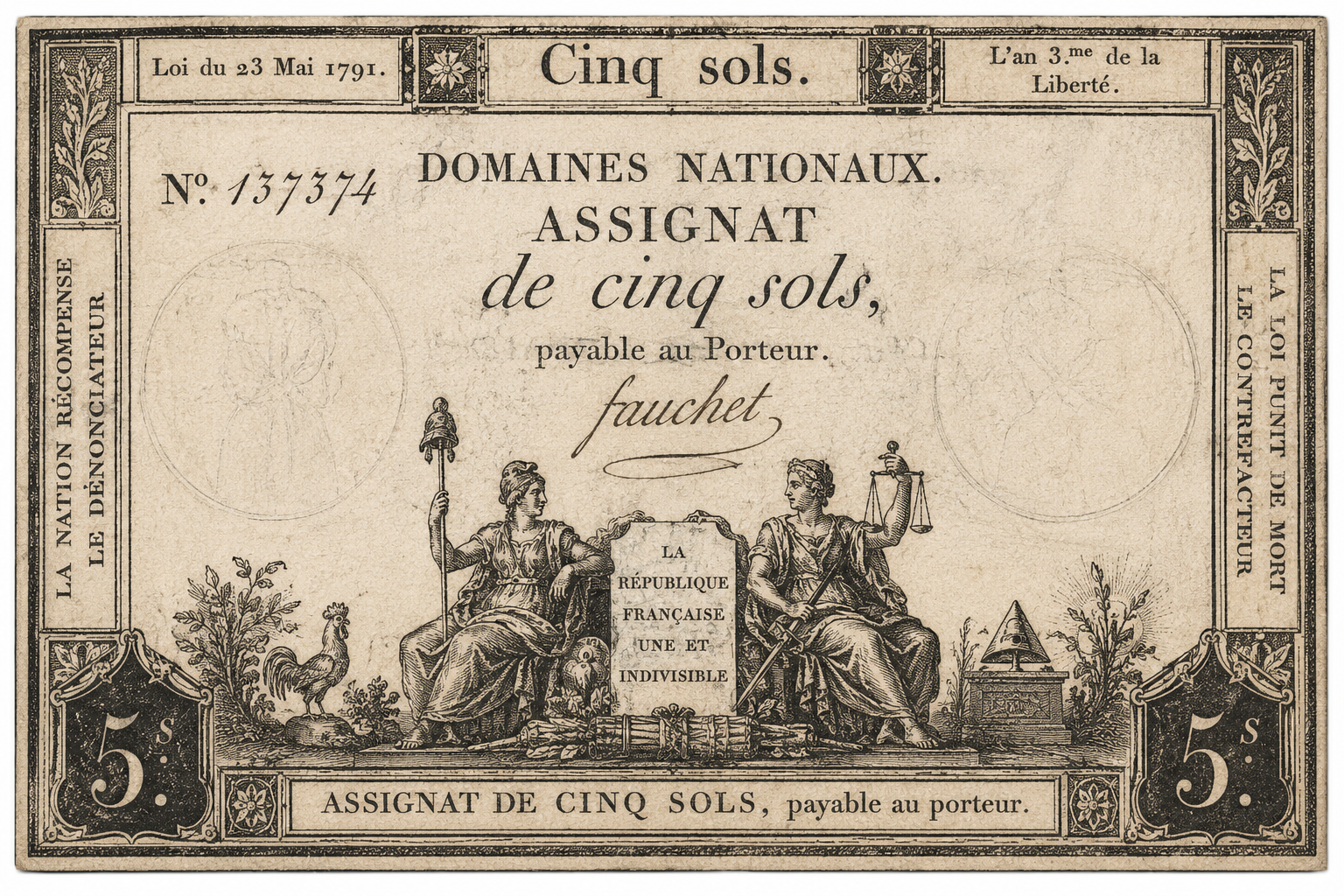

The First Modern Hyperinflation: Revolutionary France and the Assignat, 1789–1796

The world's first documented modern hyperinflation did not happen in post-war Germany. It happened in France, during the Revolution, and it is largely forgotten precisely because it was eventually overshadowed by more dramatic cases. But it is, in many ways, the purest example of how a currency system breaks down.

The French Revolutionary government inherited a bankrupt state in 1789. Unable to raise sufficient taxes, the National Assembly authorised a new paper currency called the assignat in March 1790. Initially, 400 million livres were issued, backed by the value of church lands the government had just nationalised. The principle was sound: issue paper money against a specific asset, burn the notes once the land was sold, and retire the currency. The problem was that the government needed more money faster than land could be sold.

By late 1791, 1.5 billion assignats were in circulation, and purchasing power had already declined 14%. By August 1793, the total reached 4.1 billion, and the currency had depreciated 60%. By November 1795, the figure was 19.7 billion assignats — and purchasing power had fallen 99% from the 1790 baseline. By 1796, according to the American Numismatic Society, overall prices had increased 500 times or more compared to 1790, and the total stock of assignats was 20 times the original French metallic money supply. A currency backed by a real asset had been printed into worthlessness.

The end came in February 1796, when, in a public ceremony, the printing plates for the assignat were destroyed in front of a crowd. The government attempted to replace it with a new currency called the mandat, backed by gold — but so complete was the destruction of public trust that the mandat began depreciating before it was even issued. France ultimately stabilised its currency under Napoleon, who replaced the experiment with the franc in 1803 and enforced monetary discipline by law.

Weimar Germany: The Hyperinflation That Changed the World, 1921–1923

The Weimar hyperinflation is the most studied currency collapse in history — and for good reason. Its consequences extended far beyond economics. It wiped out the savings of the German middle class, radicalised politics, and created conditions that eventually brought Adolf Hitler to power. Understanding it means understanding how a currency system, once compromised, accelerates toward total failure.

The Three Triggers

First: Germany entered the First World War by suspending gold convertibility on 4 August 1914. The gold-backed Goldmark became the paper-backed Papiermark. The government financed the war primarily through debt rather than taxes, and by 1918, Germany's national debt had ballooned to approximately 156 billion marks. The money supply had quintupled between 1914 and 1918.

Second: The Treaty of Versailles imposed reparations totalling 132 billion gold marks — equivalent to more than $500 billion today — with annual payments amounting to roughly 2.5% of German GDP. Germany did not have the foreign exchange to pay these obligations and was already running a fiscal deficit.

Third: In January 1923, France and Belgium occupied the Ruhr — Germany's industrial heartland — to seize coal and steel instead of unpaid reparations. The German government declared passive resistance and paid millions of workers to stop working. The Reichsbank financed this by printing money. By mid-1923, the government had outsourced money printing to 133 companies. The presses ran day and night.

The Numbers

The exchange rate trajectory tells the story precisely. In July 1914, one U.S. dollar bought 4.2 marks. By January 1921, it had bought 64. By July 1922, it had bought 493. By January 1923, 17,972 marks. By November 1923, at the peak of the crisis, one dollar was equivalent to 4.2 trillion marks — 1,000 billion, as Britannica records it. In October 1923 alone, monthly inflation reached 29,500%, a rate that implied prices doubling every 3.7 days.

The Human Consequences

The consequences were not abstract. Families who had saved their entire lives in Papiermarks saw those savings become literally worthless. A life insurance policy worth a comfortable retirement in 1920 could not buy a postage stamp by 1923. Workers demanded to be paid twice daily and would rush to spend wages before the afternoon's prices took hold. In the final weeks, cigarettes circulated as a more reliable currency than the official one — a textbook example of Gresham's Law operating in reverse, with sound money (cigarettes) driving out bad (marks).

The Resolution

The fix, when it came, was swift and startling. On 15 November 1923, Finance Minister Hans Luther launched the Rentenmark — a new currency backed not by gold (Germany had none) but by mortgages on all agricultural and industrial land in the country. One Rentenmark replaced one trillion Papiermarks. Crucially, the Reichsbank simultaneously stopped monetising government debt. The president of the Reichsbank, Rudolf Havenstein — who had presided over the entire catastrophe — died of a heart attack five days later. Under his successor, Hjalmar Schacht, the new currency held. The Dawes Plan of 1924 organised American loans and restructured reparations. The hyperinflation was over within weeks of the currency reform.

Hungary 1946: The Most Extreme Hyperinflation in History

Germany's 1923 hyperinflation is the most famous. But Hungary's of 1946 was, by every measurable standard, the most extreme ever recorded. In July 1946, monthly inflation reached 41.9 quadrillion per cent — that is 41,900,000,000,000,000% — a figure that remains unmatched in human history. At its peak, prices were doubling every 15.3 hours.

The causes were distinct from Germany's, but the mechanism was identical. The Second World War had destroyed an estimated 40% of Hungary's physical assets. The Soviet occupying forces removed much of what remained as war reparations. Industrial output collapsed, agricultural production failed, and tax revenues were negligible. The government printed money to pay its obligations — including, critically, Soviet reparations — and the resulting inflation fed on itself.

The Hungarian government attempted partial solutions — including a parallel indexed currency called the adópengő, whose value was adjusted by radio announcement each morning — but these proved insufficient. By July 1946, the largest denomination banknote ever officially issued for public circulation in history was the 100 quintillion pengő note (100,000,000,000,000,000,000 pengő). The resolution came on 1 August 1946, when the forint replaced the pengő at a rate of one forint for every 400,000 quadrillion pengő — that is a number with 29 zeros. International support through the IMF was essential to the stabilisation programme.

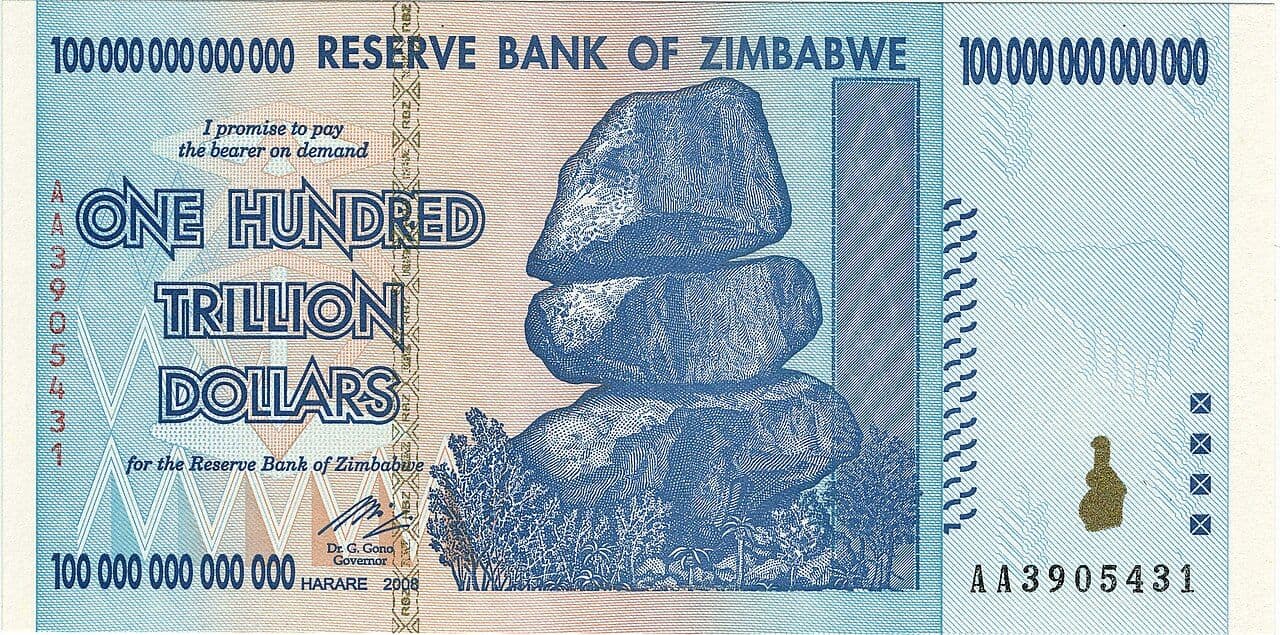

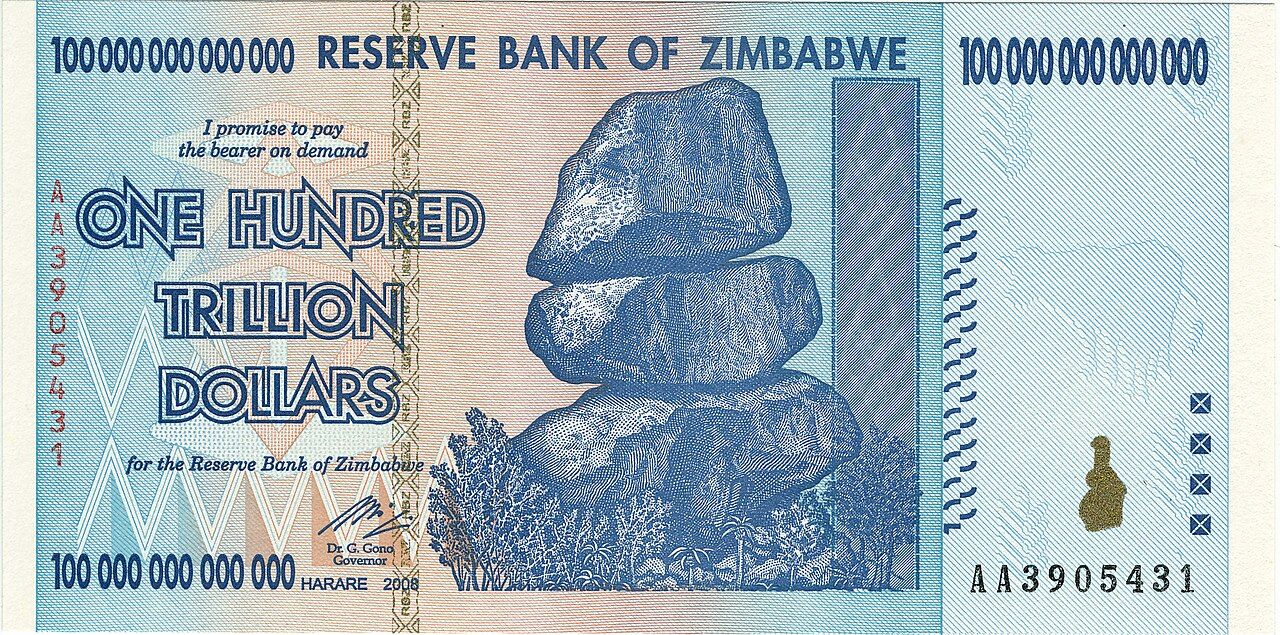

Zimbabwe 2007–2009: The Modern Collapse

Zimbabwe's hyperinflation is the best-documented modern example, and one of the most instructive precisely because it was not a post-war emergency but the result of deliberate policy choices made over a decade.

The sequence is well established. In the late 1990s, President Robert Mugabe's government implemented a fast-track land reform programme, forcibly redistributing white-owned commercial farms to black Zimbabweans. The intent was to correct colonial-era land inequality; the execution was chaotic and violent. Skilled commercial farmers were displaced, many farms were allocated to Mugabe loyalists rather than subsistence farmers, and agricultural output — Zimbabwe's main source of export revenue — collapsed. Between 1998 and 2008, GDP per capita fell from $1,640 to $661.

As export earnings evaporated and the fiscal deficit widened, the Reserve Bank of Zimbabwe turned to money printing. Price controls imposed in 2007–08 accelerated the collapse by creating shortages — businesses could not sell below cost, so they stopped selling at all. By November 2008, annual inflation was measured at 89.7 sextillion per cent (that is 89,700,000,000,000,000,000,000%). A German printing company was reportedly receiving more than €500,000 a week to supply Zimbabwe with banknotes. The $100 trillion Zimbabwe dollar note — which could not buy three eggs by the time it was issued — became one of the most iconic symbols of monetary failure in history.

The resolution came in February 2009 when Zimbabwe abandoned its dollar entirely and adopted a basket of foreign currencies — primarily the U.S. dollar — as legal tender. Inflation stopped almost immediately. But the cost was total monetary sovereignty. Zimbabwe has since attempted to reintroduce domestic currency, with limited success. The reintroduction of the Zimbabwe dollar in 2019 triggered a new inflationary spiral.

The Anatomy of Currency Collapse: What Every Case Has in Common

Across four centuries and four countries, the mechanism is consistent enough to be described as a pattern rather than a series of accidents. Every hyperinflation moves through identifiable stages — and understanding them is what makes the history useful rather than merely dramatic.

How Hyperinflation Ends: The Three Routes to Stabilisation

A credible new anchor

The most successful stabilisations have involved replacing the destroyed currency with one backed by a credible, tangible anchor. Germany's Rentenmark used land mortgages because there was no gold. The principle worked because it was finite and verifiable — the government could not simply print more land. The key condition was not what the anchor was, but that it was believable and that the central bank simultaneously stopped financing government deficits.

Dollarisation or foreign currency adoption

When institutional credibility is too far gone to support a domestic currency reform — as in Zimbabwe — governments have adopted a stronger foreign currency. The advantage is immediate stabilisation. The cost is permanent loss of monetary sovereignty: the country cannot adjust interest rates, cannot use exchange rate policy, and cannot act as lender of last resort to its own banking system.

External anchor with international support

Hungary's 1946 forint required IMF and allied-nation support to function. Contemporary stabilisations — Argentina multiple times, Turkey, various African economies — have often involved IMF programmes that combine monetary reform with fiscal adjustment. The political cost of these programmes (austerity, structural adjustment) has made them deeply controversial, even when the economics have been straightforward.

What This Means Today

The conditions for hyperinflation are specific

Modern economies with independent central banks, deep domestic bond markets, and credible fiscal institutions are not at serious risk of hyperinflation from normal monetary policy. The quantitative easing programmes of 2008–2021 expanded money supplies dramatically without triggering hyperinflation — because the underlying fiscal position remained credible and money creation was sterilised rather than financing government deficits directly. The lesson is not that printing money always causes hyperinflation; it is that printing money to cover an unsustainable fiscal position, with no credible path to correction, always does.

Political collapse precedes monetary collapse

In every historical case, the currency system did not collapse on its own. It collapsed because the political institutions responsible for managing it had lost authority or independence. The Reichsbank under Havenstein printed money because it had no political backing to refuse. The Reserve Bank of Zimbabwe printed money because Mugabe's government stripped it of independence. The French Revolutionary government printed assignats because it faced existential military threats on all sides. The currency failure is always a symptom of a deeper institutional failure.

The memory of hyperinflation is itself an economic force

Germany's experience of 1923 shaped Bundesbank policy for the rest of the century, producing a conservative monetary culture that eventually influenced the design of the European Central Bank. The ECB's mandate — price stability as the primary objective, explicit prohibition on monetary financing of government deficits — is a direct institutional response to the Weimar experience. The memory of hyperinflation, encoded in institutions and law, is one of the most durable legacies of monetary history.

Frequently Asked Questions

What is the currency system behind hyperinflation?

Hyperinflation occurs when a government with an unsustainable fiscal deficit begins financing that deficit by instructing the central bank to create money. As the money supply expands faster than economic output, prices rise. Rising prices increase the government's nominal expenditure, requiring further money creation. The feedback loop accelerates until citizens lose confidence in the currency and begin spending or converting it as fast as they receive it. Every confirmed hyperinflation in history — all 57 documented cases — has involved government deficit monetisation as the primary mechanism.

What is the definition of hyperinflation?

Economist Philip Cagan defined hyperinflation as a monthly inflation rate exceeding 50%. At 50% monthly inflation, prices double approximately every 50 days. In the worst historical episodes, prices doubled far faster: every 3.7 days in Weimar Germany at peak (October 1923), every 15.3 hours in Hungary (July 1946), and approximately every 24.7 hours in Zimbabwe (November 2008).

Which country has experienced the worst hyperinflation in history?

Hungary in 1946 holds the record for the most extreme hyperinflation ever measured. Monthly inflation in July 1946 reached 41.9 quadrillion per cent — 4.19 × 10¹⁶% — with prices doubling every 15.3 hours. The largest denomination banknote ever officially issued was the Hungarian 100 quintillion pengő note. The currency was replaced by the forint on 1 August 1946, at an exchange rate of one forint for every 400,000 quadrillion pengő.

How did Weimar Germany end hyperinflation?

Germany ended its 1923 hyperinflation through two simultaneous actions: the introduction of the Rentenmark on 15 November 1923, backed by mortgages on all German agricultural and industrial land, and the Reichsbank's decision to stop monetising government debt. One Rentenmark replaced one trillion Papiermarks. The inflation halted within weeks. The Dawes Plan of 1924 subsequently provided American loans, restructured reparations, and enabled lasting stabilisation.

Why did Zimbabwe experience hyperinflation?

Zimbabwe's 2007–09 hyperinflation resulted from a chain of policy failures. Fast-track land reform from 1999 onwards destroyed commercial agriculture and collapsed export revenues. The resulting fiscal deficit was financed by money printing. Price controls in 2007–08 created shortages and eliminated formal market activity. By November 2008, annual inflation had reached an estimated 89.7 sextillion per cent. The government abandoned its own currency in 2009 and adopted the U.S. dollar.

Can hyperinflation happen in developed economies today?

Hyperinflation in modern developed economies with independent central banks and credible fiscal institutions is extremely unlikely. The quantitative easing programmes after 2008 expanded money supplies without causing hyperinflation because the money creation was not directly financing government deficits beyond the capacity to service them. Hyperinflation requires a specific set of conditions: an unsustainable fiscal position, loss of central bank independence, and collapse of public trust in the currency. These conditions have not been present in the U.S., Eurozone, or UK in the post-war era.

What is the fastest way to stop hyperinflation?

The most effective route is a credible currency reform combined with the immediate cessation of deficit monetisation. Germany's Rentenmark worked in weeks because the Reichsbank stopped printing money at the same time the new currency was launched. The anchor does not have to be gold — land, foreign currency reserves, or an IMF-backed stabilisation programme can all work. What is essential is that the public believes the new currency will not be debased. Without that belief, as France discovered with the mandat in 1796, even a gold-backed replacement can fail immediately.