The economic collapse of Weimar Germany began as a balance-sheet problem and ended as a crisis of belief. A defeated state tried to pay for war, reparations, welfare, industrial disruption and political survival with a currency the public trusted less each week. By late 1923, ordinary Germans no longer treated the mark as money in the full sense. Wages were rushed from the pay office to the shop counter. Savings built over decades became paper. Prices changed faster than households could plan. The tragedy was not simply that Germany printed too much money. It was that the republic lost the fiscal, political and institutional credibility that makes money work in the first place.

Quick Answer: What Caused the Economic Collapse of Weimar Germany?

The economic collapse of Weimar Germany was caused by the interaction of war debt, reparations, weak tax capacity, political instability, external pressure and uncontrolled money creation. The republic inherited the financial damage of the First World War, faced reparations demands under the post-war settlement, and lacked the political strength to impose a durable fiscal settlement. When France and Belgium occupied the Ruhr in January 1923 after German defaults, the government supported passive resistance by paying workers and firms while output fell. That widened the fiscal gap and pushed the Reichsbank deeper into monetary financing.

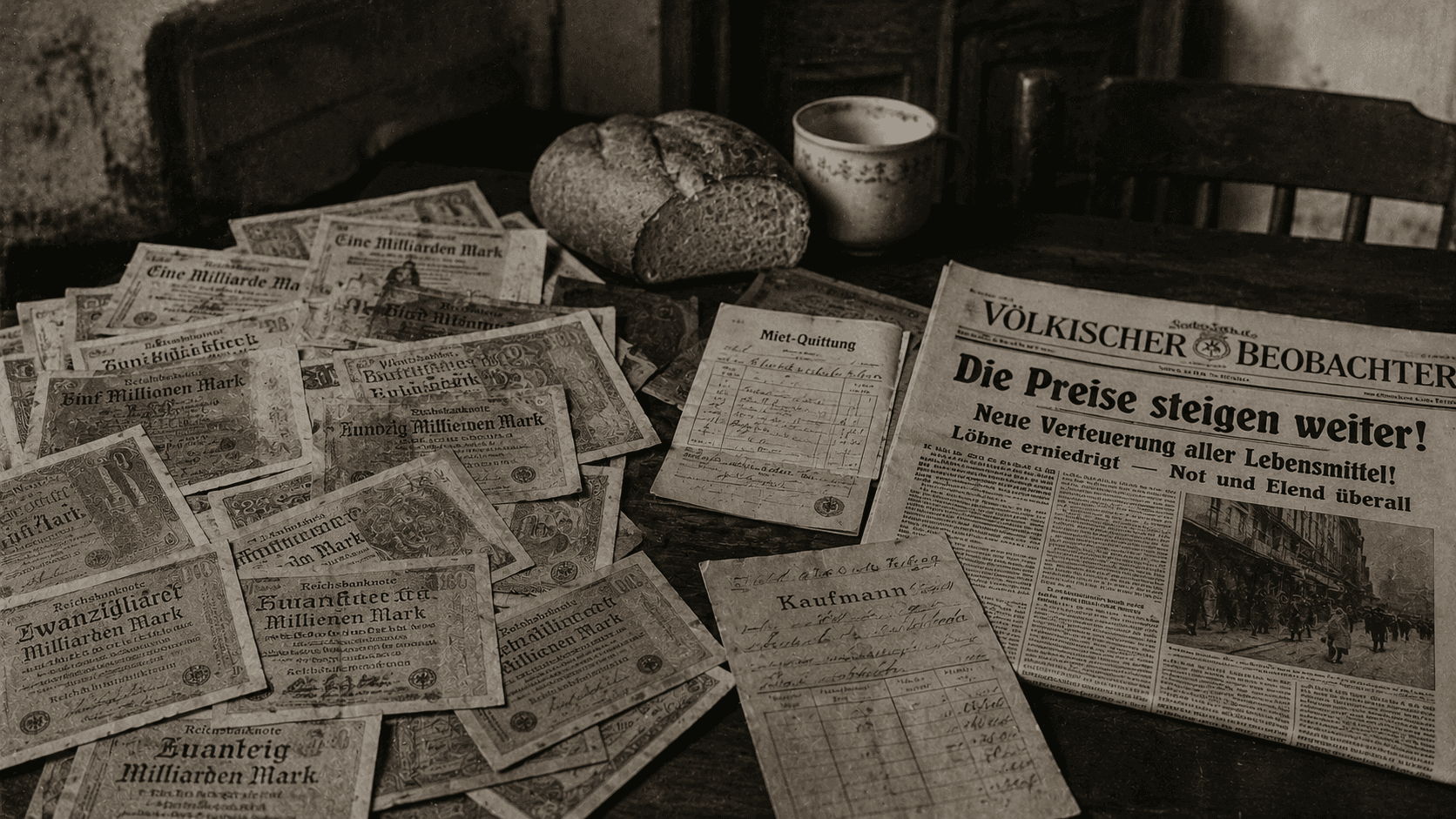

The collapse became visible through hyperinflation. Britannica records the mark falling to 160,000 to the U.S. dollar on 1 July 1923, 242 million on 1 October and 4.2 trillion by 20 November. Bundesbank describes 1923 as the moment when wages were paid daily, and people rushed to exchange notes for goods before prices moved again. The crisis ended only when the government stopped passive resistance, introduced the Rentenmark in November 1923, imposed fiscal discipline and restored confidence through new monetary rules.

The Republic Was Born With a Broken Balance Sheet

To understand Weimar Germany, we need to begin before Weimar itself. Imperial Germany did not fund the First World War through a clean, tax-heavy settlement. It leaned heavily on borrowing, expecting victory to make the financial burden manageable. Defeat reversed that logic. Instead of making others pay, Germany had to absorb domestic war debt, social disruption, demobilisation costs and the political shock of a new democratic republic blamed by many Germans for a defeat it had inherited rather than caused.

That mattered because money depends on the state behind it. A currency is not only paper, metal or entries in a bank ledger. It is a claim on a political order that can tax, borrow, enforce contracts and maintain confidence. Weimar entered office with weak legitimacy, strained public finances and enemies on both the left and right. It had to pay soldiers, civil servants, welfare costs and reparations while rebuilding a society that did not yet agree on the republic itself.

War finance became peacetime fragility

The German state had accumulated obligations during the war, but the new republic could not simply reset the ledger. Citizens held claims, businesses needed working capital, and political parties fought over who should bear the cost. Raising taxes aggressively risked deepening unrest. Cutting spending risked alienating workers, veterans and the middle classes. Borrowing depended on confidence. Printing money looked easier because it delayed the hard choice.

This is the first financial lesson of Weimar: inflation often begins when a state refuses, or cannot politically manage, a distributional conflict. Someone had to pay for the war and the peace. The state chose a path that made the cost appear gradually through the currency. That choice did not destroy the mark overnight, but it weakened the habit of believing that the mark would hold value tomorrow.

Reparations Turned a Fiscal Problem Into an International Crisis

The reparations question made the Weimar economy more fragile by converting domestic weakness into an international payment problem. The Treaty of Versailles created the framework, and the 1921 London Schedule of Payments fixed the machinery for securing Germany's reparation obligations. The political argument inside Germany was explosive: many Germans saw reparations as punitive, while the Allied powers viewed them as compensation for the destruction of war.

The financial issue was harder than the headline number. Germany could print marks, but reparations required resources that creditors would accept: goods, foreign exchange, coal, timber or other transfers of value. Printing more domestic currency did not automatically create foreign exchange. As the mark weakened, the external burden became harder to manage. The weaker the currency became, the more expensive foreign obligations felt in domestic terms, and the more desperate the fiscal position looked.

The politics of payment undermined the politics of reform

A credible stabilisation programme would have required unpopular choices: taxation, spending cuts, monetary restraint and acceptance of external constraints. Weimar governments struggled to hold together parliamentary coalitions long enough to make that settlement stick. In a calmer country, reparations might have been renegotiated earlier around realistic capacity. In Weimar, every attempt to pay or compromise could be attacked as surrender; every refusal invited foreign pressure.

The result was a bad loop. Reparations weakened the budget. The weak budget encouraged money creation. Money creation weakened the mark. A weak mark deepened the sense that Germany was being squeezed by forces beyond its control. Political anger then made fiscal discipline even harder. The collapse was not mechanical. It was institutional.

The Ruhr Crisis Turned Inflation Into Hyperinflation

January 1923 was the decisive escalation. After Germany fell behind on reparations deliveries, French and Belgian troops occupied the Ruhr, Germany's industrial heartland. The German response was passive resistance: workers were encouraged not to cooperate with the occupation authorities, and the government supported them financially. This was politically understandable. It was also economically disastrous.

The Ruhr was not a symbolic region. It was central to coal, steel and industrial output. When production was disrupted, the state's revenues weakened, and the supply of goods tightened. At the same time, the government paid idle workers and subsidised affected firms. In simple terms, fewer goods were being produced while more paper claims were being issued. The mark was asked to carry a burden that the real economy could no longer support.

Passive resistance had a monetary bill

The phrase passive resistance can make the policy sound costless. It was not. Workers still had to eat. Families still needed rent money. Firms still needed support. Civil servants are still expected to be paid. Because the state lacked enough tax revenue and market confidence, the costs were pushed towards the central bank and the printing press. The Bundesbank notes that by 1923, the currency fell so quickly that wages were paid daily in many places, with people carrying notes in bags and suitcases to buy goods before prices rose again.

Here, the story becomes human. A salary was no longer a stable promise; it was a melting block of ice. A pension was not a lifetime of security; it was a number losing meaning. A shopkeeper had to decide whether to price goods for the morning, the afternoon or the next delivery. Money normally coordinates strangers. In Weimar Germany, it stopped coordinating time.

The Mark Lost Its Function as Money

Money performs three basic tasks: it works as a medium of exchange, a unit of account and a store of value. Weimar's mark failed all three. It could still be handed over in transactions, but only if accepted quickly. It could still quote prices, but those prices were revised with frantic frequency. It could still sit in a bank account, but it no longer preserves command over future goods.

That is why hyperinflation is more destructive than high inflation. High inflation damages planning. Hyperinflation destroys the measurement system. Contracts written in marks became arbitrary. Debtors could repay old obligations with worthless currency. Creditors and savers were wiped out. Wage earners with frequent pay adjustments could survive better than people on fixed incomes, but even they were trapped in a race against prices. Those with real assets, foreign currency, inventories or access to hard goods had protection. Those holding cash savings were exposed.

Wealth was redistributed at speed

The collapse of the mark was also a redistribution event. Savers lost. Some debtors gained because nominal debts could be extinguished in depreciated marks. Workers with bargaining power fought for wage adjustments. Pensioners, clerks and the lower middle class were often crushed. The crisis, therefore, did not simply reduce national wealth evenly. It changed who owned claims on the future.

This matters because political memory is shaped by perceived injustice. The Weimar hyperinflation created stories of betrayal: the prudent saver punished, the speculator rewarded, the household budget humiliated, the shop price made absurd. Even after stabilisation, the memory remained. Economic collapse is never only about output and prices. It is about whether citizens believe the system treats sacrifice and prudence with respect.

Political Extremes Fed on Economic Humiliation

Weimar Germany did not collapse politically in 1923, but the economic crisis damaged the republic's credibility. The German Historical Museum describes the occupation of the Ruhr, inflation and economic crisis as threats to the cohesion of the young republic. The U.S. Holocaust Memorial Museum presents Weimar as a twelve-year democratic experiment that ended when the Nazis came to power in January 1933. The line between the 1923 crisis and the 1933 dictatorship was not straight or inevitable, but the economic trauma weakened democratic trust.

The hyperinflation gave extremists a powerful narrative. The republic could be portrayed as weak, humiliated and financially incompetent. Foreign creditors, domestic politicians, bankers, profiteers and minorities could be folded into conspiracy stories. A population that had watched money lose meaning was more willing to believe that the whole political system was fraudulent. The economy did not create extremism from nothing, but it supplied grievance, fear and evidence that normal institutions had failed.

The middle-class wound was especially deep

The social danger came from the groups who believed they had played by the rules. Civil servants, pensioners, small savers and salaried professionals depended on money claims and fixed incomes. They did not hold enough land, foreign currency or inventories to protect themselves. Inflation, therefore, felt like a moral inversion: thrift was punished, and speculation appeared rational. In political terms, that is combustible.

This is why Weimar still matters for financial history. The crisis shows that monetary collapse can change the emotional map of a society. It can make moderate reform look weak, make technical policy feel like betrayal, and make radical simplicity sound attractive. A currency collapse is a political education, and in Weimar, that education was brutal.

The Rentenmark Stopped the Panic Because It Changed the Rules

The end of the crisis came not from one magic note but from a credible regime shift. Gustav Stresemann's government ended passive resistance in the Ruhr. Fiscal policy was tightened. The Rentenmark was introduced in November 1923, backed not by available gold but by claims tied to land and industrial assets. The Reichsbank was restrained from continuing the same open-ended financing of government deficits. The public did not need the new currency to be perfect. It needed proof that the old rules had been broken.

The Bundesbank summarises the reform directly: the government introduced currency reform by replacing the Mark with the Rentenmark in November 1923 after inflation had almost completely devalued financial assets and liabilities denominated in marks. Britannica records the extreme exchange-rate collapse before stabilisation, and its Dawes Plan entry explains that the 1924 arrangement reorganised the Reichsbank and included an initial loan of 800 million marks. Stabilisation, therefore, combined domestic monetary reform with external restructuring.

Credibility was the real backing

It is tempting to say the Rentenmark succeeded because it was backed by land. That was important symbolically and institutionally, but the deeper point is credibility. The public believed that issuance would be limited and that the government had changed course. A currency is backed by assets only if the legal and political system around those assets is believable. The Rentenmark worked because it was part of a wider change in fiscal and monetary behaviour.

This is the second financial lesson of Weimar: stabilisation requires a story the public can verify. A government cannot merely announce confidence. It has to demonstrate constraint. It must show that deficits will not simply be passed to the central bank, that money creation will have limits, and that future policy will differ from the policy that caused the collapse.

The Dawes Plan Brought Relief, but Also New Dependency

After the currency was stabilised, Weimar entered a period often remembered as relatively calm. The Dawes Plan, accepted in 1924, restructured reparations payments and helped restore access to foreign lending. Britannica notes that the plan provided for Reichsbank reorganisation and an initial loan of 800 million marks. This mattered because Germany needed breathing space. Stabilisation without external finance would have been harsher and politically harder.

Yet the recovery carried a vulnerability. Weimar became dependent on foreign capital, especially short-term flows linked to the broader international financial system. This did not cause the 1923 hyperinflation, but it shaped the next crisis. When the Wall Street Crash and global depression hit after 1929, Germany was exposed again. The same republic that had survived hyperinflation then faced mass unemployment, banking pressure and collapsing confidence.

Weimar had two economic traumas, not one

The popular memory of Weimar often compresses the story into wheelbarrows of money and the rise of Nazism. That is too simple. Weimar endured hyperinflation in 1923 and then depression after 1929. The first destroyed savings and confidence in money. The second destroyed jobs and confidence in democratic capitalism. Together, they created a devastating sequence: first, the currency failed, then employment failed.

For readers of financial history, the distinction is vital. Hyperinflation is not the same as depression, and the policies that stop one can aggravate or fail to solve the other. Weimar's tragedy was that it experienced both within a single democratic lifetime. Citizens were asked to trust institutions that had already failed them once.

What This Means Today

The economic collapse of Weimar Germany still matters because it shows how quickly money can become political. Modern economies are not Weimar. They have deeper tax systems, independent central banks, deposit insurance, broader capital markets and far more developed policy tools. But the underlying lesson remains sharp: currency stability depends on the credibility of institutions, not on paper alone.

Central banks need independence, but governments need discipline

Weimar is often used as a warning about central banks printing money. That warning is valid but incomplete. The deeper issue was the fiscal state behind the central bank. When governments rely on monetary financing because they cannot tax, borrow or cut spending credibly, the central bank becomes the instrument of political failure. Modern central-bank independence is designed to prevent the collapse of boundaries.

Inflation is also a trust problem

People accept money because they believe others will accept it tomorrow. Once that belief breaks, technical tools alone may not be enough. Weimar shows that inflation expectations are social as well as statistical. Workers, shopkeepers and savers act on what they think the state will do next. Credibility is therefore not a slogan. It is a policy asset.

Debt sustainability is a political question before it is a spreadsheet question

A debt burden is sustainable when a society accepts the taxes, spending choices and growth strategy needed to service it. Weimar lacked that settlement. The republic could not align domestic politics, external obligations and monetary restraint. Modern states should read Weimar less as a prediction and more as a boundary marker: when fiscal promises outrun institutional trust, money becomes the pressure valve.

Frequently Asked Questions

What caused the economic collapse of Weimar Germany?

The collapse was caused by war debt, reparations pressure, weak tax capacity, political instability and money-financed deficits. The Ruhr occupation in 1923 intensified the crisis because the government paid for passive resistance while industrial output fell.

Was Weimar hyperinflation caused only by reparations?

No. Reparations mattered, but they were not the only cause. The crisis also reflected Germany's war-finance legacy, budget deficits, political weakness, central-bank financing and the Ruhr crisis.

When did Weimar hyperinflation peak?

The hyperinflation peaked in late 1923. Britannica records the mark falling to 4.2 trillion to the U.S. dollar by 20 November 1923.

How did Germany stop hyperinflation in 1923?

Germany stopped hyperinflation by ending passive resistance in the Ruhr, tightening fiscal policy, limiting monetary financing and introducing the Rentenmark in November 1923.

What was the Rentenmark?

The Rentenmark was the stabilisation currency introduced in November 1923 after the Papiermark had become effectively worthless. It was backed by claims linked to land and industrial assets and, more importantly, by a new policy regime that limited issuance.

Did Weimar Germany recover after the collapse?

Germany stabilised after 1923 and experienced a period of relative recovery under the Dawes Plan. However, that recovery depended heavily on foreign capital and was badly exposed when the global depression hit after 1929.

Why does Weimar Germany still matter today?

Weimar matters because it shows that inflation can become a political and social crisis when fiscal credibility collapses. It remains one of history's clearest examples of how monetary failure can damage savings, contracts, institutions and trust.