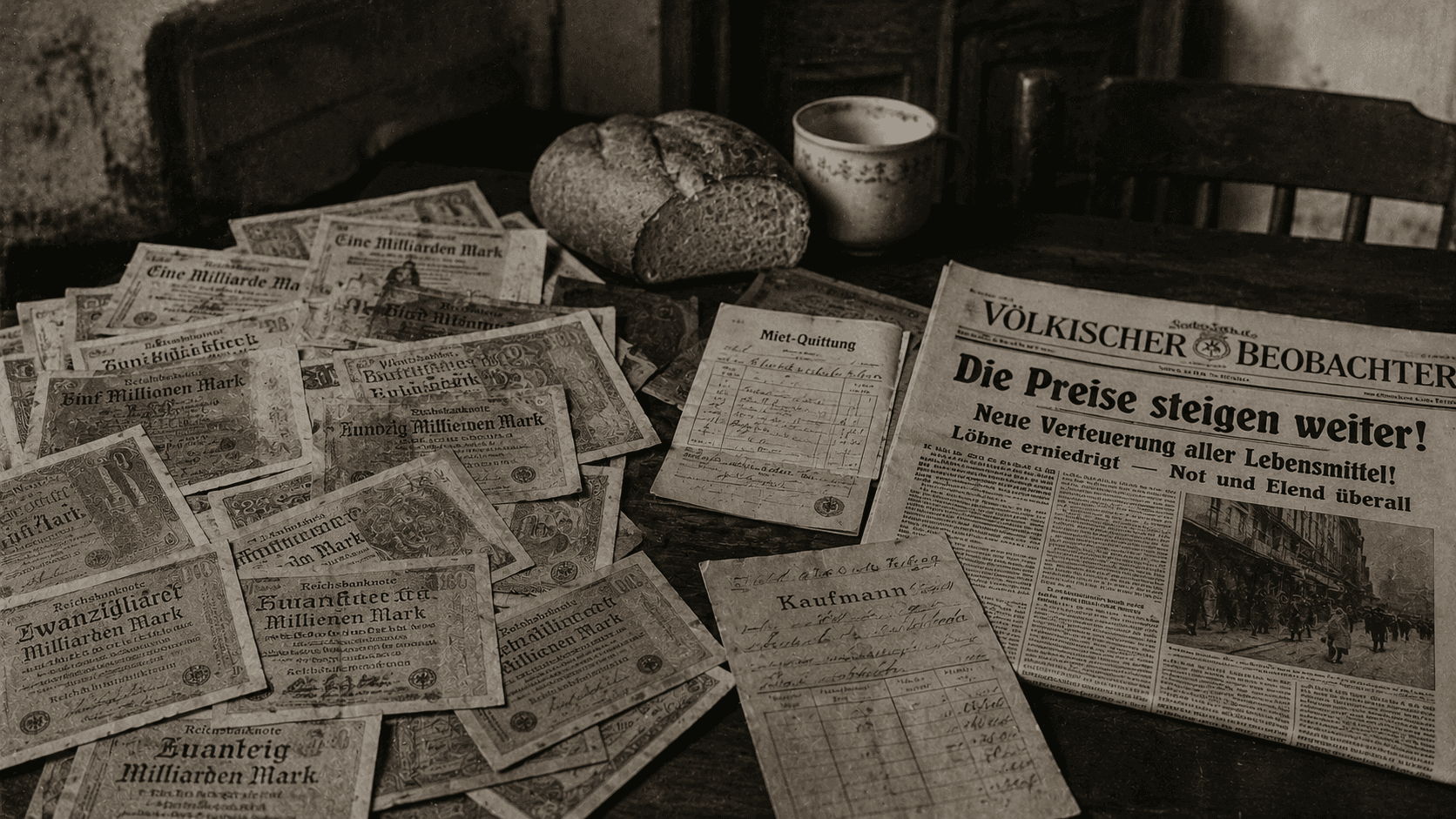

By mid-2008, it took Z$100 billion to buy three eggs. The Reserve Bank of Zimbabwe was printing Z$100 trillion notes — the largest denomination banknote ever issued for public circulation in history — and they were worthless within weeks of leaving the press. At the peak of the crisis in November 2008, annual inflation was estimated at 89.7 sextillion per cent: that is 89,700,000,000,000,000,000,000%. Prices were doubling approximately every 24 hours. Unemployment had reached 80%. Eight out of every ten Zimbabweans who still had formal employment by 2007 had lost it.

This was not a natural disaster. It was not a war or an invasion. It was the endpoint of a decade-long chain of policy decisions — each one compounding the damage of the last — that destroyed first the agricultural economy, then the fiscal position, then the currency, and finally the institutional credibility on which any currency depends.

Zimbabwe's hyperinflation is the most instructive modern example of what happens when a currency collapses — not because it is the most extreme (Hungary in 1946 holds that record) but because it unfolded slowly enough, and was documented thoroughly enough, that we can trace every link in the chain from first cause to final destruction. This is that story.

The Beginning: Black Friday and the 1997 Turning Point

Zimbabwe's economic story before the crisis was not one of chronic failure. At independence in 1980, the Zimbabwe dollar launched at parity with the US dollar — a position of genuine strength, reflecting a productive economy. The country had strong commercial agriculture producing tobacco, maize, cotton, and other export crops. It had a functioning manufacturing sector, a literate workforce, and a legal system that, for Africa at the time, was relatively well-developed.

The first decisive break came in November 1997 — a date Zimbabweans call Black Friday. Under pressure from war veterans demanding recognition for their service in the liberation struggle, President Mugabe announced unbudgeted payouts worth Z$4.5 billion. The announcement was made without consulting the Finance Ministry or the Reserve Bank. International investors, who had been watching the government's fiscal position deteriorate, lost confidence immediately. Foreign capital fled. In a single day, the Zimbabwe dollar lost 75% of its value against the US dollar.

The Reserve Bank's foreign reserves — the buffer that a central bank uses to defend the currency in foreign exchange markets — were exhausted. The government responded by reimposing import controls and banning foreign currency accounts: emergency measures that signalled to the world that Zimbabwe's monetary management had broken down.

The Engine of Destruction: Fast-Track Land Reform

The 1997 currency shock was serious but potentially recoverable. What made it the beginning of a decade-long catastrophe was what followed: the fast-track land reform programme beginning in 2000.

The historical injustice was real. In 1980, most of Zimbabwe's most fertile commercial farmland was owned by a small number of white settlers, leaving millions of Black Zimbabweans landless. A gradual land reform programme had been underway since independence, but it was slow and expensive — the government had to buy land at market prices under the Lancaster House Agreement. By the late 1990s, pressure from war veterans and rural communities for accelerated redistribution had become a defining political issue.

In early 2000, encouraged by government promises and the apparent absence of police intervention, hundreds of white-owned farms were invaded and occupied by war veterans. The government legalised and accelerated these seizures. Between 2000 and 2001, nearly all commercial farming land was expropriated and redistributed — not, in most cases, to landless subsistence farmers but to political loyalists, military officers, and members of the ruling ZANU-PF party, many of whom had no farming experience.

The economic consequences were immediate and catastrophic. Commercial agriculture had provided an estimated 38% of Zimbabwe's total foreign exchange earnings. With the displacement of skilled commercial farmers, that revenue was gone almost overnight — an estimated 90% of foreign exchange earnings from farming were lost under the reform programme. Food output fell 45% between 1999 and 2008. Manufacturing, which depended on imported inputs paid for with agricultural export earnings, fell 29% in 2005, 26% in 2006, and 28% in 2007.

The Fiscal Trap: Printing Money to Fill the Gap

With export earnings gone, the government faced an impossible fiscal position. It had commitments — civil service salaries, military expenditure, subsidies, debt service — that it could no longer fund from tax revenue, because the tax base was collapsing along with the economy. It could not borrow at affordable rates in international markets because Zimbabwe's credit rating had been destroyed by its debt arrears and the land seizures.

The only remaining tool was the Reserve Bank of Zimbabwe's printing press. Between 2000 and 2008, the government financed its budget deficit almost entirely through money creation. The money supply expanded at an accelerating rate. More money chasing a shrinking quantity of goods produced rising prices. Rising prices required more nominal government expenditure to maintain the same real services. Higher nominal expenditure required more money for printing. The feedback loop was identical to every other hyperinflation in history.

The additional dimension in Zimbabwe's case was the Congo War. From 1998, Zimbabwe deployed troops to the Democratic Republic of Congo in support of President Kabila — a costly military commitment that consumed foreign exchange and added to fiscal pressure at precisely the moment the agricultural export base was collapsing. Critics argued the war was also a source of personal enrichment for connected military and political figures, further undermining the legitimacy of the fiscal position.

Price Controls: The Policy That Made Everything Worse

As inflation accelerated in 2007, the government introduced statutory price controls — setting maximum legal prices for basic goods. The intention was to prevent businesses from "profiteering" from the crisis. The effect was the reverse.

When the official price of a loaf of bread is set below the cost of the flour, yeast, and energy required to make it, rational producers stop making bread. Businesses cannot sell below cost and survive, so they stop selling. Shops that had stock stopped restocking it. Shelves emptied. A parallel black market emerged in which goods were available — but only at prices far above the official rates, denominated in US dollars rather than Zimbabwe dollars.

By September 2007, the black market was the only functioning market. Press reports described ordinary Zimbabweans who had been earning the equivalent of US$11 a month in formal employment, finding that black market trading could earn them US$166 a month. The formal economy had ceased to function. By 2007, formal employment had disappeared for eight out of ten people. The emigration rate rose from 6% of the population in 2005 to 9.9% by 2010 as hundreds of thousands fled to South Africa, the United Kingdom, and elsewhere.

The Peak: 89.7 Sextillion Per cent

Economist Steve Hanke of Johns Hopkins University, who tracked Zimbabwe's inflation using black-market exchange rate data, established that Zimbabwe crossed the technical definition of hyperinflation (50% monthly inflation by Cagan's standard) in February 2007. From that point, the trajectory was consistent: accelerating at an accelerating rate, with no corrective policy intervention capable of breaking the momentum.

By November 2008, the monthly inflation rate was estimated at 79.6 per cent — meaning prices roughly doubled every 24.7 hours. Annual inflation, extrapolated from this, was approximately 89.7 sextillion per cent. These numbers are so large that they lose intuitive meaning. The practical reality was described in human terms: people who received wages in the morning spent them immediately before they lost value by afternoon. Employers paid workers twice daily. Shops changed price tags by hand several times a day.

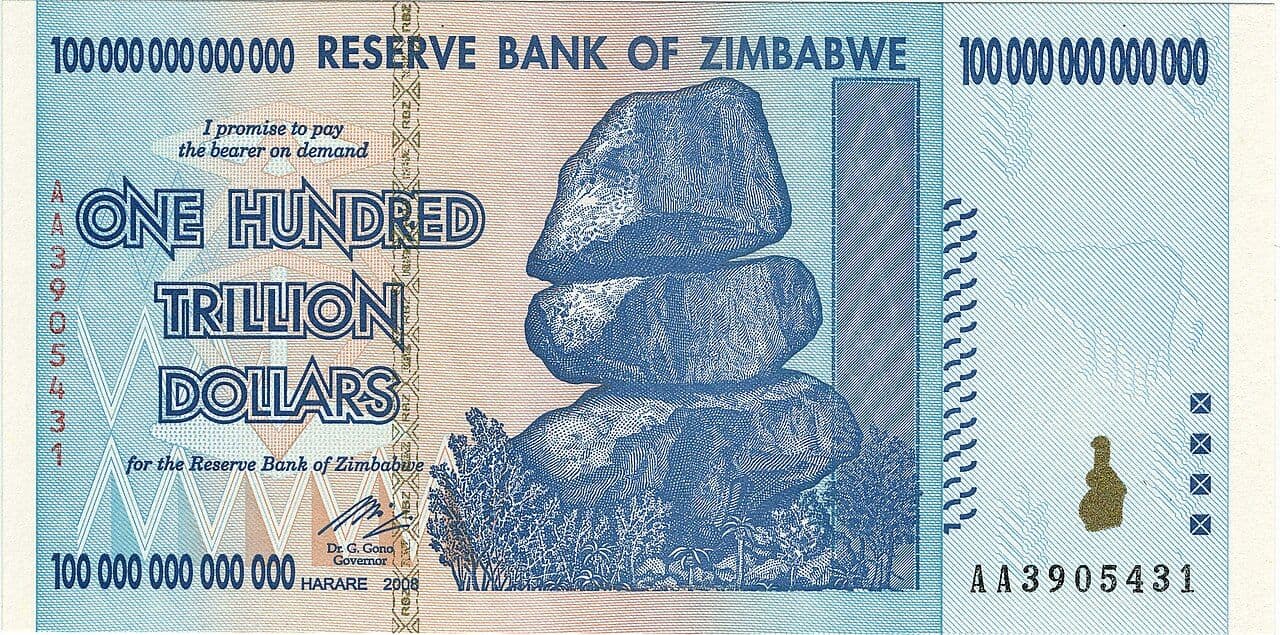

In January 2009, Reserve Bank Governor Gideon Gono authorised the issue of the Z$100 trillion note — 100,000,000,000,000 Zimbabwe dollars — the largest denomination ever officially issued for public circulation. The note was intended to ease a cash shortage caused by the collapse of the monetary system. It could not buy a loaf of bread within weeks of issue. The exchange rate at the point of formal dollarisation in February 2009 stood at Z$35 quadrillion to the US dollar — that is 35,000,000,000,000,000 Zimbabwe dollars per dollar.

Dollarisation: How It Ended and What It Cost

In February 2009, the Government of National Unity — a power-sharing arrangement between Mugabe's ZANU-PF and Morgan Tsvangirai's Movement for Democratic Change — formally adopted a multicurrency system. The Zimbabwe dollar was demonetised. US dollars, South African rand, Botswana pula, and other foreign currencies became legal tender. The printing press stopped. Inflation stopped almost immediately.

The recovery, measured by simple inflation statistics, was dramatic. Inflation fell from the incalculable levels of 2008 to around 4.3% by July 2018. Shops restocked. The formal economy partially resumed. But the cost of stabilisation was total: Zimbabwe had surrendered its monetary sovereignty entirely. It could not set interest rates. It could not use the exchange rate policy. It could not act as a lender of last resort to its own banking system. Its fiscal policy was constrained by the physical availability of US dollar cash, which gradually dried up over the decade as more dollars flowed out of Zimbabwe than came in.

Six Currencies, Zero Trust: The Post-2009 Failure

Since 2009, Zimbabwe has attempted to reintroduce a domestic currency six times. Each attempt has failed — not because the currency was technically poorly designed, but because institutional trust, once destroyed at the scale of 89.7 sextillion per cent inflation, cannot be restored by announcement.

Bond coins (2014) and bond notes (2016) were introduced as substitutes for US dollar change, officially at 1:1 parity. They immediately traded below par on the black market. The RTGS dollar (February 2019) was a virtual currency based on Zimbabwe's interbank payment system; it lasted four months before being merged into a new Zimbabwe dollar (ZWL). The ZWL lost 80% of its value against the US dollar and was abandoned in April 2024.

In April 2024, the government introduced Zimbabwe Gold (ZiG) — the sixth attempt — backed by 2.5 tonnes of physical gold and $100 million in cash reserves. The design is more credible than its predecessors. But as of writing, public trust remains limited. Zimbabweans who lived through the 2008 crisis, and who have watched five subsequent currencies fail, approach each new note with scepticism that no announcement can dissolve.

What This Means Today

Hyperinflation is always the endpoint of a policy chain, not a single event

Zimbabwe's collapse was not caused by printing money. It was caused by a sequence: land reform destroyed export earnings → export collapse destroyed the fiscal base → fiscal collapse led to money printing → money printing caused inflation → price controls caused shortages → shortages caused social breakdown → breakdown required more printing. Each step followed rationally from the last, given the political constraints on the government. Understanding this matters because it means hyperinflation always has a policy history — and that history can, in principle, be read in advance.

Institutional credibility takes decades to build and minutes to destroy

Zimbabwe's dollar launched at parity with the US dollar in 1980 based on genuine economic strength. That credibility was accumulated over years of productive governance. It was destroyed through Black Friday in 1997, then the land reform, then money printing, in under a decade. Rebuilding it has proved vastly harder than destroying it. Six currencies later, Zimbabweans still prefer US dollars for any significant transaction. The lesson: institutional trust cannot be manufactured. It can only be demonstrated through consistency over time.

Monetary sovereignty is not absolute

Zimbabwe's dollarisation ended its hyperinflation instantly — but at the cost of complete loss of monetary independence. This trade-off recurs across every hyperinflation stabilisation: Ecuador dollarised in 2000, and Panama has used the dollar since 1904. The benefit is credibility borrowed from the anchor currency. The cost is the permanent inability to respond to domestic economic shocks with monetary tools. For Zimbabwe, which needed to rebuild an entire productive base, the absence of any ability to manage the exchange rate or set interest rates has constrained recovery significantly.

The parallel economy is always the honest one

Throughout Zimbabwe's crisis, the parallel market — the black market in US dollars, gold, and barter — continued to price goods accurately even as official statistics and official currencies became meaningless. This is a consistent feature of hyperinflationary economies: formal markets fail, but informal markets persist, denominated in whatever medium of exchange people actually trust. The informal economy does not eliminate the damage of hyperinflation — it merely reveals it honestly, stripping away the fiction of official prices.

Frequently Asked Questions

What caused Zimbabwe's hyperinflation?

Zimbabwe's hyperinflation resulted from a chain of policy failures over a decade. The fast-track land reform from 2000 destroyed commercial agriculture and collapsed export earnings by an estimated 90%. The resulting fiscal deficit — with a shrinking tax base and ongoing military expenditure — was financed by Reserve Bank money printing. Price controls in 2007–08 eliminated formal markets and caused shortages. By November 2008, monthly inflation reached 79.6 billion percent and annual inflation was estimated at 89.7 sextillion per cent.

How bad was Zimbabwe's hyperinflation at its peak?

At its November 2008 peak, Zimbabwe's monthly inflation rate was approximately 79.6 billion per cent — meaning prices doubled roughly every 24.7 hours. The annual rate was estimated at 89.7 sextillion per cent (89,700,000,000,000,000,000,000%). The largest denomination banknote ever issued for public circulation, the Z$100 trillion note, was issued in January 2009 and was worthless within weeks. The exchange rate at dollarisation was Z$35 quadrillion per US dollar.

When did Zimbabwe abandon its dollar?

Zimbabwe formally demonetised the Zimbabwe dollar in February 2009, adopting a multicurrency system with the US dollar, South African rand, and other foreign currencies as legal tender. This ended hyperinflation almost immediately. The formal demonetisation of old Zimbabwe dollar notes followed in 2015, when any remaining Z$ notes could be exchanged for US dollars at a rate of Z$35 quadrillion per US dollar.

How many currencies has Zimbabwe had since 2009?

Zimbabwe has attempted six different currency arrangements since 2009: the multicurrency/dollarisation system (2009–2019), bond coins (2014), bond notes (2016), the RTGS dollar (February–June 2019), the new Zimbabwe dollar/ZWL (2019–2024), and Zimbabwe Gold/ZiG (April 2024 onwards). Each domestic currency attempt has failed to gain public trust, with Zimbabweans consistently preferring US dollars for significant transactions.

What was the role of land reform in Zimbabwe's economic collapse?

Fast-track land reform from 2000 was the pivotal economic event. Commercial farming had provided approximately 38% of Zimbabwe's foreign exchange earnings; the rapid and chaotic dispossession of skilled commercial farmers collapsed that revenue by an estimated 90%. Food output fell 45% from 1999 to 2008. The loss of export earnings eliminated the government's ability to service foreign debt and import essential inputs, triggering a fiscal crisis that was ultimately financed by money printing.

How does Zimbabwe's hyperinflation compare to others in history?

Zimbabwe's 2008 episode was the second most extreme hyperinflation ever recorded. Hungary's July 1946 hyperinflation remains the worst, with monthly inflation reaching 41.9 quadrillion per cent and prices doubling every 15.3 hours. Zimbabwe's peak monthly rate of 79.6 billion per cent and doubling time of approximately 24.7 hours is more severe than Weimar Germany's October 1923 peak (29,500% monthly, doubling every 3.7 days), making it second only to Hungary in modern monetary history.

Can Zimbabwe's dollar ever recover?

Currency credibility, once destroyed at the scale Zimbabwe experienced, can only be rebuilt through years of demonstrated fiscal discipline and monetary restraint — not through the design of any particular currency. Zimbabwe Gold (ZiG), launched in April 2024 with gold and cash backing, represents the most credible attempt since dollarisation. But trust will be rebuilt incrementally through consistent policy, not through an announcement. The history of five previous failed attempts is an active constraint on public confidence in any successor currency.