In the 1970s, Venezuela was one of the top 20 richest countries in the world. Its oil revenues funded universal healthcare, education, and social programmes that made it the envy of Latin America. Caracas was a cosmopolitan city of glass towers, imported goods, and a middle class that could afford to holiday in Miami. The country sat on top of the world's largest proven oil reserves — a geological endowment so vast it seemed to guarantee prosperity in perpetuity.

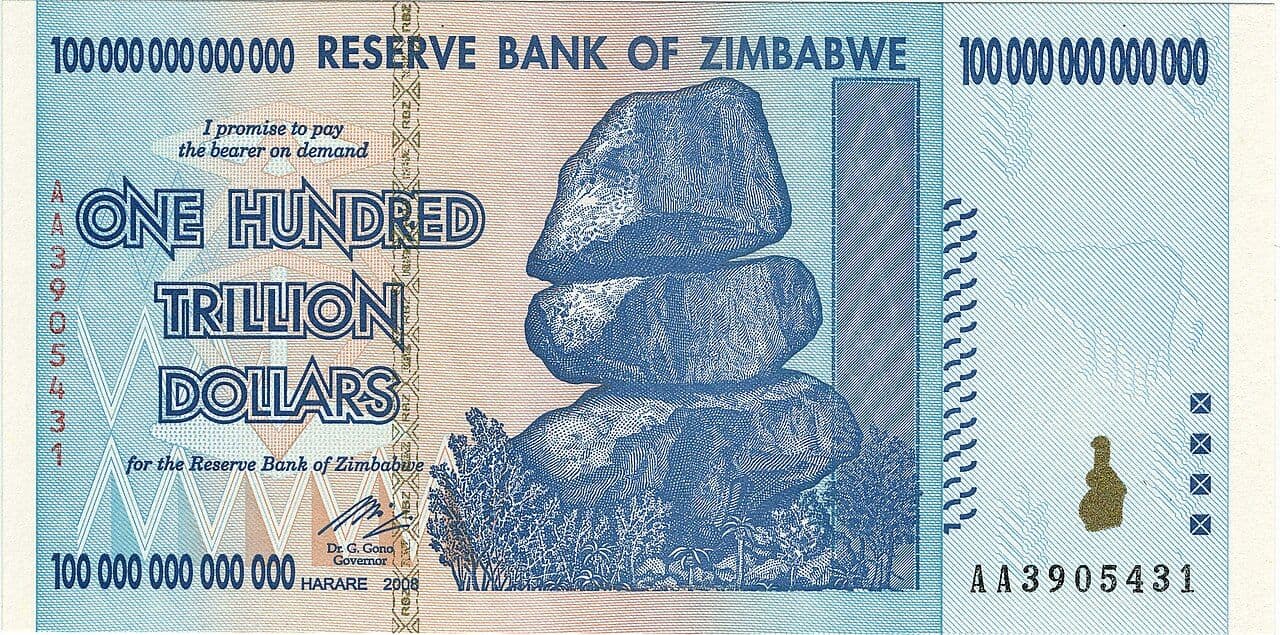

Between 2013 and 2021, Venezuela's economy shrank by approximately 75–80%. That contraction is deeper than the one the United States suffered in the Great Depression. It is larger than the Soviet Union's collapse. Annual inflation reached 130,060% in 2018 by the government's own central bank figures — and independent estimates were significantly higher. Nearly 8 million Venezuelans, approximately 15% of the population, fled the country. The Bolívar — the national currency — had 14 zeros stripped from it in three separate redenominations over 13 years. None of those redenominations stopped the inflation, because none of them addressed its cause.

This is not a story about a country without resources. It is a story about what happens when resources become a trap — when oil wealth enables a government to avoid fiscal discipline, destroy productive capacity, manipulate exchange rates, and finally print money at scale when the oil price falls. Venezuela is the definitive modern case study of the petrostate pathology.

The Petrostate Trap: Building a Nation on One Price

Venezuela's vulnerability began long before Chávez. The country had been a petro-state since oil was discovered in 1922, a nation whose fiscal position moved entirely with the oil price. When prices were high, governments spent. When prices fell, they borrowed. The classic dysfunction economists call Dutch disease — where resource revenues inflate the currency, pricing out all other exports and leaving only oil — had been developing for decades.

When Hugo Chávez was elected in 1998, oil accounted for roughly 71% of Venezuela's export revenues. By 2013, the year Chávez died and Nicolás Maduro inherited the presidency, fuel constituted approximately 97.7% of Venezuela's merchandise exports. That is not an economy with oil as its leading sector. That is an economy that had ceased to have any other meaningful sector at all.

The non-oil economy — manufacturing, agriculture, services — had been systematically hollowed out. Chávez's government expropriated hundreds of private businesses and foreign-owned assets, including oil projects operated by ExxonMobil and ConocoPhillips, deterring investment. Strict currency controls imposed in 2003 to prevent capital flight overvalued the Bolívar, making Venezuelan non-oil goods uncompetitive internationally. Price controls on domestic goods made production unprofitable, reducing supply. Each of these policies seemed politically rational in isolation. Together, they eliminated the productive diversity that might have buffered against an oil price shock.

PDVSA: Destroying the Engine

The most consequential single decision in Venezuela's economic history was made in 2002–2003. When PDVSA workers joined a nationwide general strike against Chávez, the government responded by firing over 18,000 employees — geologists, reservoir engineers, technical managers, and specialists who had spent careers understanding Venezuela's complex heavy-oil fields.

These were not easily replaceable. Oil production, particularly from Venezuela's Orinoco Belt extra-heavy crude, requires deep institutional knowledge — understanding of reservoir pressures, well casing conditions, and injection programmes. The fired workers were replaced with political loyalists who lacked the technical expertise to manage a capital-intensive oil industry. As Asia Times analysis put it, PDVSA stopped injecting water and gas into ageing wells to maintain pressure. The result was a production freefall from approximately 3 million barrels per day in the late 1990s to a nadir of under 500,000 barrels per day by 2020.

Simultaneously, PDVSA's revenues were redirected from capital reinvestment into social programmes and subsidised oil exports — to Cuba (in exchange for doctors and teachers), and to other Latin American countries through the Petrocaribe alliance at below-market rates. Oil revenue that should have maintained the infrastructure of Venezuela's productive base was instead spent on consumption and political relationships. The consequence was infrastructure decay that was irreversible without massive foreign investment.

The Boom That Was Squandered

From 2005 to 2013, global oil prices were elevated — frequently above $100 per barrel. For a country with Venezuela's production, this was an extraordinary windfall. The question was what to do with it.

The answer, for both Chávez and Maduro, was to spend it all. Norway, Saudi Arabia, and virtually all other major oil exporters had established sovereign wealth funds to save at least a portion of boom-time revenues for the inevitable price corrections. Venezuela did not. According to the Economics Observatory analysis, the government ran double-digit fiscal deficits even during the boom years, spending far beyond tax and oil revenues. To finance these shortfalls, Venezuela raised external debt by approximately sixfold, saddling the government and PDVSA with over $100 billion in obligations by the time the crisis hit.

The social programmes funded by this spending were real. Poverty fell by some 20% during Chávez's presidency. Literacy programmes, healthcare clinics, and food subsidies reached millions. But the funding mechanism was entirely unsustainable: it was consumption financed by borrowing, not growth financed by investment. The moment the oil price fell, there was no cushion, no alternative revenue base, no sovereign fund, and no creditworthiness left to borrow more.

The Oil Price Collapse: When Everything Broke

In mid-2014, global oil prices fell sharply — from over $100 per barrel in the summer to below $50 by early 2015, and briefly under $33 in early 2016. For Venezuela, this was not a manageable cyclical shock. It was an existential crisis.

Imports — which Venezuela depended on for 70% of its consumer goods, given the destruction of domestic production — collapsed from over $80 billion in 2012 to approximately $10 billion by 2017. GDP contracted 17% in 2016 and 16% in 2017. These are not recession figures. They are depression figures. Despite this, Maduro refused to rationalise economic policy. Subsidies were maintained. The military and political apparatus continued to be funded. Price controls that had already distorted markets for a decade remained in place.

With tax revenues collapsing alongside oil earnings and no access to international credit markets, the government turned to the only remaining tool: the Central Bank of Venezuela's printing press. The central bank, by this point, had no meaningful independence from the government. It functioned, in the words of Asia Times analysis, as "a printing press for the Ministry of Finance." The money supply expanded 20–30% per month. Venezuela crossed the technical threshold for hyperinflation in November 2016.

Price Controls, Shortages, and the Parallel Economy

Venezuela's price control history illustrates a pattern that recurs in every hyperinflation: governments impose legal price ceilings on goods to prevent "profiteering," and the result is that goods disappear from formal markets.

When the controlled price of basic food is below the cost of producing and distributing it, rational producers stop producing it. When the controlled exchange rate values the Bolívar far above its real market value, importers cannot access the foreign currency needed to bring in goods at the official rate — and the goods stop arriving. The black market, denominated in US dollars or barter, becomes the only functioning market. By 2016–2018, Venezuelans were queuing for hours to access state-subsidised food bags, and even those were frequently unavailable.

A platform called Dolar Today — tracking black-market dollar exchange rates from Miami — became the de facto price reference for Venezuela's economy. The government periodically threatened to prosecute its operators for "economic warfare." The reality was simpler: Dolar Today was publishing honest prices in a country where official prices had become fiction. By 2022, over 60% of Venezuelan transactions were conducted in US dollars informally — dollarisation that happened from below, without government authorisation, because it was the only way commerce could function.

The Bolívar and 14 Zeros: Redenomination as Theatre

As inflation accelerated, the government engaged in a series of currency redenominations — removing zeros from the Bolívar to make it more manageable to count. The Bolívar Fuerte replaced the Bolívar in 2008, removing three zeros. The Bolívar Soberano replaced it in 2018, removing five more zeros. The Bolívar digital replaced that in 2021, removing six more zeros. In total, 14 zeros were removed in 13 years.

These redenominations had no economic effect whatsoever. Inflation continued at the same rate before and after each one. Removing zeros from a currency does not change the underlying money supply dynamics, the fiscal deficit, or the government's propensity to print. It simply shifts the decimal point while the printing continues. Asia Times analysis accurately characterised them as "purely cosmetic accounting adjustments that failed to restore the store of value function of money."

In 2018, the government also launched the "Petro" — a state-backed cryptocurrency supposedly pegged to Venezuela's oil reserves, designed to bypass U.S. sanctions and access international finance. It failed almost immediately. There was no transparent backing mechanism, it could not be traded on international exchanges, and no rational investor was prepared to hold an asset backed by the promise of a government in the middle of hyperinflation. The Petro was quietly dismantled.

The Human Cost: 8 million Refugees

The statistics of Venezuela's collapse are large enough to become abstract. The human reality was the largest migration crisis in the Americas. Since 2014, nearly 8 million Venezuelans — approximately 15% of the population — fled the country, primarily to Colombia, Peru, Ecuador, Chile, and Brazil.

At the peak of the crisis, poverty affected over 90% of the population. Food insecurity and malnutrition became serious public health crises. Medicines disappeared from hospitals. The healthcare system that Chávez had built with oil revenues collapsed when those revenues were gone. A November 2022 survey found 50% of Venezuela's 28 million residents still lived in poverty — and this was after partial recovery from the worst years.

The emigration represented a severe brain drain on top of the physical economic destruction. Doctors, engineers, teachers, and skilled workers who left took with them precisely the human capital that any recovery would require. Venezuela had already gutted PDVSA of its technical expertise in 2003. Two decades later, the broader economy had been similarly hollowed out by emigration — creating a compounding human capital crisis that will constrain any recovery for decades.

Informal Dollarisation and the Fragile Stabilisation

The stabilisation that has partially occurred since 2021 did not come from successful government policy. It came from below: the informal dollarisation of the economy. As Venezuelans and businesses increasingly transacted in US dollars, the Bolívar became irrelevant to daily commerce. Dollar pricing removed the government's ability to erode real wages and savings through inflation — because savings were no longer held in Bolívares.

By 2022, this informal dollarisation had slowed inflation significantly. Modest GDP growth of 4–5% occurred in 2023–2024, partly from Chevron's resumed oil operations under limited U.S. sanctions relief. But this was growth from a devastated base. Indexing 2013 GDP at 100, Venezuela would require decades of sustained expansion to recover to its pre-collapse output. Oil production, at around 800,000 barrels per day in 2023, remained 73% below its late-1990s peak.

What This Means Today

Resource wealth without institutional restraint is a curse

The "resource curse" or Dutch disease is well-documented in economic literature, but Venezuela is its most extreme modern expression. Resource wealth is not inherently destructive — Norway's Government Pension Fund holds over $1.7 trillion and was built from oil revenues. The difference is institutional restraint: rules that prevent governments from spending windfalls, that require saving in boom years, and that protect the non-resource economy from currency overvaluation. Venezuela had none of these. Every rule was a constraint that Chávez's government removed.

Fiscal dominance destroys monetary systems

When a government loses the ability or willingness to fund itself through taxation and borrowing and begins instead instructing the central bank to create money, the monetary system is subordinated to fiscal necessity. Economists call this "fiscal dominance" — and it is the mechanism behind every hyperinflation in history, from Weimar Germany to Zimbabwe to Venezuela. The central bank becomes a revenue department rather than a monetary authority. Independence is not a technocratic nicety: it is the structural barrier between monetary policy and fiscal desperation.

Price controls accelerate the breakdown that they are meant to prevent

Venezuela's experience reinforces what every hyperinflationary episode shows: price controls do not suppress inflation, they redirect it. Suppressed official prices eliminate formal markets. The informal market — which prices honestly — takes over. The government then faces the worst of both worlds: official markets that don't function, and informal markets it cannot tax or control. The political temptation to impose controls is understandable. The economic consequence is always the same.

Human capital is the hardest thing to rebuild

PDVSA's firing of 18,000 technicians in 2003 was recoverable in theory — those people existed. By 2024, Venezuela had lost millions of its most educated and skilled citizens to emigration, its oil company's institutional knowledge was gone, its healthcare system had collapsed, and its education infrastructure had deteriorated. Physical capital — oil wells, refineries, buildings — can be rebuilt with investment. Human capital, accumulated over generations, takes generations to restore. Venezuela's deepest wound may be the brain drain that its policies caused.

Frequently Asked Questions

What caused Venezuela's economic collapse?

Venezuela's collapse resulted from compounding policy failures: extreme oil dependence (97.7% of exports by 2013), the systematic destruction of PDVSA's technical capacity by firing 18,000 skilled workers in 2003, expropriations that eliminated domestic productive capacity, fiscal deficits run even during the oil boom, currency controls that overvalued the Bolívar, and finally money printing to cover fiscal deficits when oil prices collapsed in 2014. Sanctions from 2017 onwards worsened the crisis but were not its primary cause.

How bad was Venezuela's hyperinflation?

Venezuela crossed the 50% monthly inflation threshold (Cagan's definition of hyperinflation) in November 2016. Annual inflation reached 130,060% in 2018 according to the government's own Central Bank of Venezuela data; independent estimates were higher. The Bolívar had 14 zeros stripped from it in three redenominations between 2008 and 2021, none of which stopped inflation because none changed the underlying money-printing dynamic.

How much did Venezuela's economy shrink?

Between 2013 and 2021, Venezuela's GDP contracted by approximately 75–80% — a contraction larger than the United States suffered in the Great Depression (29%) and comparable to the Soviet Union's collapse. Imports fell from over $80 billion in 2012 to approximately $10 billion in 2017. Oil production collapsed from approximately 3 million barrels per day in the late 1990s to under 500,000 barrels per day by 2020.

How many Venezuelans fled the country?

Since 2014, nearly 8 million Venezuelans — approximately 15% of the total population — have fled the country, primarily to Colombia, Peru, Ecuador, Chile, and Brazil. This is the largest migration crisis in the Americas, comparable in proportional scale to the Syrian refugee crisis. At the peak of the economic collapse, poverty affected over 90% of the population.

Did U.S. sanctions cause Venezuela's economic collapse?

U.S. sanctions, imposed progressively from 2017 with the most severe PDVSA sanctions in 2019, worsened and prolonged the crisis significantly. However, the evidence clearly shows that Venezuela's economic collapse — the inflation spiral, the production collapse, the food shortages — was well underway before broad sanctions were imposed. PDVSA's production had been declining for years due to technical mismanagement predating any sanctions. The fiscal deficit, money printing, and hyperinflation threshold were all crossed before 2019.

What is informal dollarisation, and how did it stabilise Venezuela?

Informal dollarisation is the spontaneous adoption of a foreign currency (primarily the US dollar) for everyday transactions, without formal government authorisation. By 2022, over 60% of Venezuelan transactions were conducted in US dollars. This stabilised the economy partially because it removed the Bolívar from most commercial transactions, limiting the government's ability to inflate away real purchasing power. The formal economy partly resumed, and inflation slowed significantly — though it remained extremely high by international standards.

What lessons does Venezuela teach about oil-dependent economies?

Four lessons stand out: (1) Resource wealth requires institutional rules to prevent pro-cyclical spending — save during booms. (2) Productive diversification must be maintained even when commodity revenues make it seem unnecessary. (3) Central bank independence is a structural safeguard against fiscal dominance, not a technocratic preference. (4) Human capital — the skilled workforce — is the most valuable and most difficult to replace asset in any economy; destroying it through ideological purges and creating emigration incentives has consequences that outlast the political crisis by generations.