The untold financial history of the Great Depression is not simply the story of a stock market crash; it is the story of a financial system that lost the ability to protect trust. Behind the famous images of Wall Street panic, bank queues and mass unemployment was a deeper chain reaction: falling asset prices weakened collateral, frightened depositors withdrew cash, banks contracted credit, prices fell, debts became heavier, and the gold standard restricted the monetary response. This article follows the money through that chain. We will look beyond the usual surface narrative and examine how banking, credit, deflation, trade and regulation turned a severe downturn into the defining financial crisis of the twentieth century.

Quick answer: What was the untold financial history of the Great Depression?

The untold financial history of the Great Depression is that the crisis was less a single stock market event than a full-system failure of credit, banking, money and policy. The crash of October 1929 damaged confidence, but the Depression became catastrophic because banks failed, deposits disappeared, money contracted, prices fell, debts became harder to repay and international trade seized up.

The deeper lesson is that financial systems are built on confidence. Once households no longer trust banks, banks no longer trust borrowers, and governments defend old monetary rules instead of stabilising the system, an ordinary downturn can become a depression. The Great Depression revealed how modern capitalism depends on credible money, liquid banks, deposit protection and policy flexibility.

By 1933, the United States was no longer dealing with a normal recession. It was dealing with a monetary contraction, a banking panic and an institutional legitimacy crisis at the same time. The emergency reforms that followed did not simply restart growth. They rebuilt the architecture of modern finance.

The financial boom before the collapse

To understand the Great Depression, we need to begin with the financial optimism of the 1920s. The United States entered the decade with rising industrial output, expanding consumer credit, wider share ownership and a cultural belief that prosperity had become self-sustaining. That confidence mattered because it changed behaviour. Households borrowed more freely, businesses planned around growth, and investors increasingly treated asset prices as proof of economic strength.

The financial system was not yet designed for that scale of speculation. Securities markets had limited disclosure standards compared with the rules that later developed after the New Deal. Banks were fragmented across thousands of institutions, many of them small and geographically exposed. Deposit insurance did not yet exist at the federal level. A depositor who feared a bank might fail had a rational incentive to withdraw cash before everyone else did.

That structure made the boom fragile. Rising share prices created paper wealth, but paper wealth is not the same as resilient capital. When confidence turned, falling stock prices damaged collateral values, damaged household balance sheets and made lenders more cautious. The market crash was the visible break, but the hidden vulnerability was the amount of economic activity that depended on easy credit and uninterrupted trust.

The stock market crash was the spark, not the whole fire

The crash of October 1929 remains the most famous image of the Great Depression because it was dramatic, measurable and public. On Black Monday, 28 October 1929, the Dow Jones Industrial Average fell nearly 13%. On Black Tuesday, 29 October, it fell by nearly another 12%. By mid-November, the index had lost almost half its value, and by the summer of 1932, it stood 89% below its peak.

Those figures are severe, but they do not explain the whole Depression by themselves. Stock markets can crash without creating a decade-long economic disaster. The reason 1929 became different is that the crash exposed weaknesses in the credit system. Investors who had borrowed against securities faced margin pressure. Banks with exposed customers and declining assets became more cautious. Businesses that expected continuing demand cut investment. Households that believed prosperity was permanent began to preserve cash.

The immediate financial effect was psychological as well as mechanical. A falling market told the public that the future had changed. Once that belief spread, spending and lending contracted together. That is where the financial history becomes more important than the market history. The Depression was not simply about the price of equities. It was about what happened when collapsing asset prices collided with weak banks, debt-heavy borrowers and a monetary regime that constrained the response.

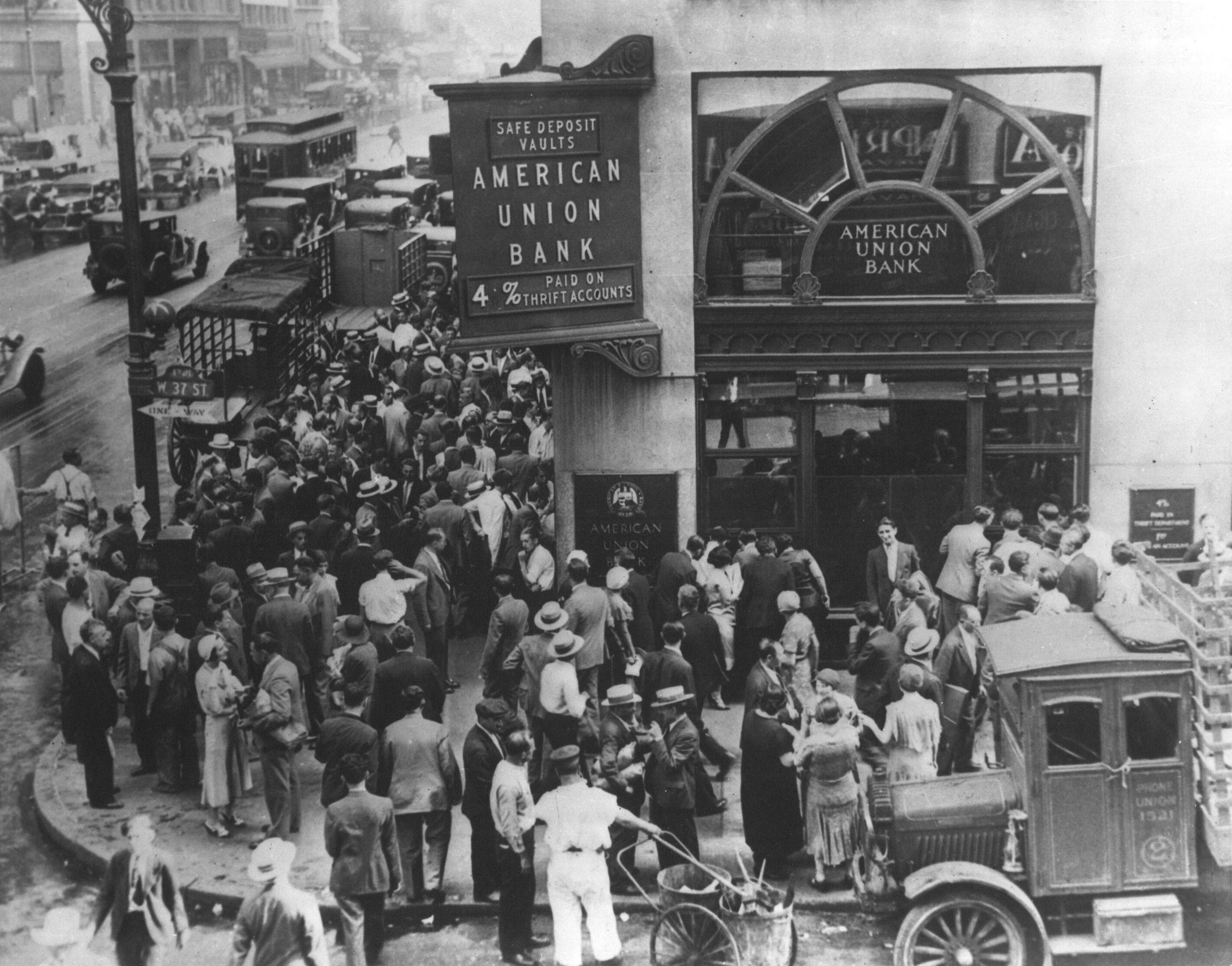

Bank runs turned fear into forced liquidation

The banking crisis is the central financial story of the Great Depression. Before federal deposit insurance, bank deposits were promises backed by public trust, bank assets and cash reserves. If enough depositors demanded cash at once, even a bank with sound long-term assets could fail because it could not instantly convert loans into currency without taking losses.

That is why bank runs became so destructive. A rumour about one bank could lead depositors to withdraw from another. Banks responded by conserving cash, selling assets, calling loans and refusing new credit. Those defensive actions protected individual institutions in the short term but damaged the wider economy. Firms lost working capital, farmers could not refinance, households lost deposits, and local communities lost their financial intermediaries.

The first major wave of bank failures in the Depression era intensified in late 1930. Further banking panics followed in 1931, 1932 and early 1933. The system reached its breaking point before Roosevelt took office in March 1933. State-level bank holidays had already appeared, and the new administration moved immediately to close the banking system temporarily, examine banks and reopen only those considered sound.

The national bank holiday worked because it changed the logic of panic. Instead of asking every depositor to decide alone whether a bank was safe, the government inserted itself as the confidence mechanism. The Emergency Banking Act and subsequent reopening process told the public that surviving banks had passed a basic test. Confidence, once broken, had to be manufactured institutionally.

Money contraction made every debt heavier

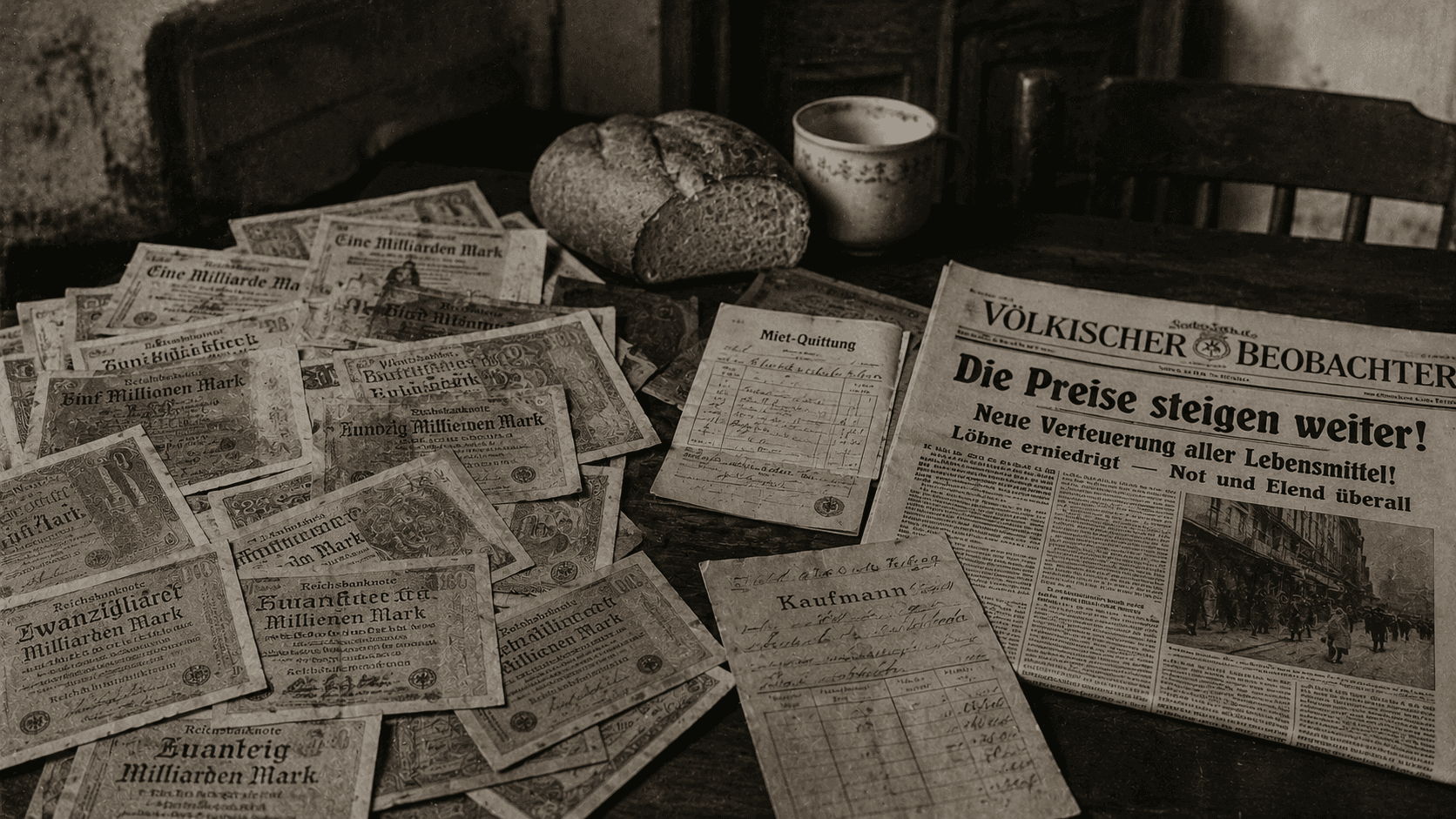

The most damaging financial mechanism was deflation. The Federal Reserve History account of the period describes the money supply falling by nearly 30% from the fall of 1930 through the winter of 1933. When the supply of money contracts, prices and incomes tend to fall. That sounds abstract until we connect it to debt.

A borrower does not owe a percentage of tomorrow’s income. A borrower owes a fixed amount of money. If wages, crop prices, business revenues and asset values fall while the nominal debt remains the same, the real burden of debt rises. A mortgage, farm loan or business loan becomes harder to service even if the interest rate has not changed. That is the core of debt deflation.

Debt deflation creates a brutal feedback loop. Borrowers sell assets to raise cash. Forced selling pushes asset prices lower. Lower prices weaken collateral. Weaker collateral makes banks less willing to lend. Reduced lending suppresses spending and investment. Lower spending pushes revenues down again. The financial system starts amplifying the downturn instead of absorbing it.

This is why the Great Depression became a monetary and balance-sheet crisis. The question was not only whether people wanted to buy goods. It was whether the financial system could keep enough money and credit circulating to prevent debts from crushing borrowers. In the early 1930s, the answer was no.

The gold standard made policy harder when flexibility was needed

The gold standard was meant to provide monetary discipline and credibility. Currencies were tied to a fixed amount of gold, and governments were expected to defend convertibility. In stable times, that framework reassured investors that money would not be casually debased. In a crisis, however, the same discipline became a trap.

A country defending gold convertibility could not freely expand money or cut rates if doing so risked gold outflows. The result was a policy bias towards austerity and monetary tightness when economies needed liquidity. Several countries transmitted deflation to one another through this mechanism. Britannica’s account notes that the American decline was transmitted to the rest of the world largely through the gold standard, although other factors also mattered.

Roosevelt’s 1933 gold programme changed that constraint. In April 1933, the United States suspended key gold standard rules, prohibited gold exports and limited the conversion of currency and deposits into gold coins and ingots. That did not instantly solve unemployment or restore all output, but it changed expectations. Once money was no longer locked into the old gold constraint in the same way, policy had more room to reflate the economy.

The financial lesson is uncomfortable but important. Credible rules can stabilise prosperity, but rigid rules can also deepen collapse. The gold standard gave investors confidence in convertibility, yet during the Depression, it restricted the very monetary expansion needed to stop deflation. Sound money became dangerous when it prevented emergency liquidity.

Protectionism spread the financial pain across borders

The Great Depression was also a global trade and payments crisis. The United States passed the Smoot-Hawley Tariff Act in 1930, raising trade barriers at a moment when demand was already weakening. The U.S. Office of the Historian states that world trade declined by about 66% between 1929 and 1934. Not all of that decline was caused by tariffs; collapsing income and credit conditions mattered heavily. But protectionism made cooperation harder and reinforced the contraction.

Trade finance depends on confidence. Exporters need buyers who can pay. Importers need credit. Banks need trust in counterparties. When international finance weakens, trade volumes fall. When trade volumes fall, producers lose markets. When producers lose markets, employment and incomes decline further. The Depression showed that trade policy is not separate from finance. It sits inside the same confidence system.

The international dimension also helps explain why recovery was uneven. Countries that escaped the gold constraint earlier often gained more room to stabilise money and prices. Countries that remained tied to restrictive monetary rules for longer faced deeper deflationary pressure. In that sense, the Great Depression was not just a domestic American failure. It was a failure of the interwar financial order.

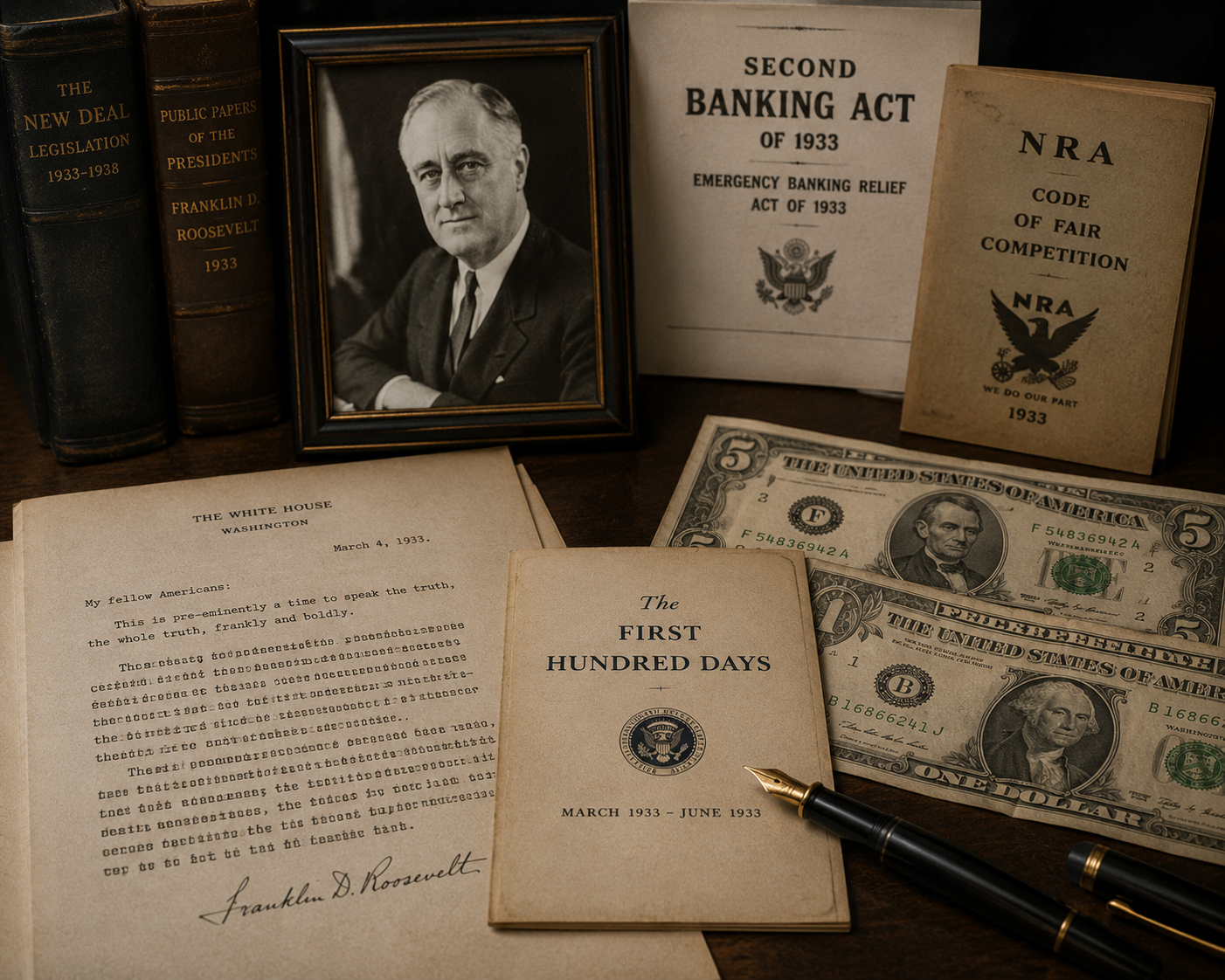

The New Deal rebuilt the financial operating system

The New Deal is often discussed as a jobs programme, a welfare programme or a political revolution. It was also a financial reconstruction project. The immediate priority was banking confidence. The national bank holiday, the Emergency Banking Act and the reopening of banks signalled that the federal government was now taking explicit responsibility for system stability.

The Banking Act of 1933, commonly associated with Glass-Steagall, separated commercial banking from investment banking and created the Federal Deposit Insurance Corporation. Federal deposit insurance became effective on 1 January 1934 with $2,500 of coverage. The FDIC’s own historical account records that only nine banks failed in 1934, compared with more than 9,000 in the preceding four years.

That change was profound. Deposit insurance altered the incentives of ordinary savers. If depositors believed insured deposits were safe, they no longer had the same reason to run at the first sign of fear. The policy did not remove every risk from banking, but it changed the public psychology of deposits. A bank account became less like an unsecured private promise and more like a protected part of the national financial infrastructure.

The reforms also reshaped the relationship between markets and the state. Securities regulation, banking supervision, deposit insurance and central bank restructuring all reflected the same lesson: financial markets need rules that preserve confidence before panic begins. The Depression did not end laissez-faire capitalism, but it ended the idea that modern finance could be left to self-correct after a systemic breakdown.

Why this financial history is still underappreciated

The popular story of the Great Depression often moves too quickly from the stock market crash to breadlines and New Deal relief. That skips the machinery in the middle. The machinery was finance: deposits, credit, money supply, collateral, international payments, tariffs, gold and public trust.

That machinery matters because it explains why the Depression became so hard to stop. If the issue had only been lower demand, fiscal spending alone might have been enough. If the issue had only been speculation, stock market rules might have been enough. If the issue had only been bad banks, closures and mergers might have been enough. Instead, the crisis connected every channel at once.

The Depression also teaches us that private balance sheets and public institutions cannot be separated. When millions of households and firms are overextended, the financial system becomes fragile. When banks are fragile, governments inherit the problem. When governments are constrained by outdated monetary rules, recovery slows. That is the real untold financial history: the Depression was a failure of the entire economic plumbing.

What This Means Today

Central banks cannot ignore money and credit transmission

Modern central banks watch inflation, employment, credit spreads, bank funding markets and financial stability because the Depression proved that money and credit are not background variables. If the banking system stops transmitting credit, policy rates alone do not tell the full story. Liquidity, collateral and confidence become just as important as headline interest rates.

Deposit confidence is a public good

Deposit insurance exists because panic can be rational at the individual level and destructive at the system level. A depositor who runs early may protect themselves, but millions doing the same thing can destroy otherwise viable banks. The modern lesson is that financial confidence often requires a credible public backstop before fear becomes self-fulfilling.

Rigid monetary rules can become dangerous in a crisis

The gold standard imposed discipline, but during the Depression, it limited flexibility when economies needed expansion. Today’s equivalent is not gold convertibility; it is any policy framework that becomes so rigid it prevents authorities from responding to systemic stress. Rules matter, but crisis rules must preserve liquidity.

Trade barriers can intensify financial stress

Smoot-Hawley Tariff remains a warning because tariffs were introduced into an already contracting global economy. Trade restrictions rarely operate in isolation. They affect prices, investment decisions, supply chains, export revenues and the political willingness of countries to cooperate when liquidity is scarce.

FAQ

What was the real financial cause of the Great Depression?

The Depression had several causes, but the central financial mechanism was the interaction between bank failures, money contraction, deflation and debt. The stock market crash damaged confidence, but the collapse of credit and deposits made the downturn much deeper.

Was the Great Depression caused only by the 1929 stock market crash?

No. The crash was a major trigger, but it was not sufficient by itself to explain the scale of the Depression. Banking panics, monetary contraction, the gold standard, falling prices and collapsing trade turned the crash into a systemic crisis.

Why did banks fail during the Great Depression?

Banks failed because depositors withdrew cash, borrowers defaulted, asset prices fell, and many banks could not liquidate assets quickly enough to meet withdrawals. Without federal deposit insurance, fear itself could destroy confidence in a local bank.

How did deflation make the Great Depression worse?

Deflation pushed prices and incomes down while debts remained fixed in nominal terms. That made loans harder to repay, forced asset sales, weakened collateral and caused banks to reduce lending further.

Why was the gold standard a problem in the Great Depression?

The gold standard restricted the ability of governments and central banks to expand money during the crisis. Defending gold convertibility encouraged tighter policy when economies needed liquidity and reflation.

What financial reforms came out of the Great Depression?

Major reforms included the Emergency Banking Act, the Banking Act of 1933, federal deposit insurance through the FDIC, securities regulation and later restructuring of the Federal Reserve system. These reforms made financial stability a central public responsibility.

What is the biggest lesson from the Great Depression for today?

The biggest lesson is that financial confidence must be protected before panic spreads. Once banks, money, trade and household balance sheets deteriorate together, recovery becomes far harder and more expensive.